Twitter feed of company looks somewhat genuine, with lots of investors cursing them  https://twitter.com/8KMiles

https://twitter.com/8KMiles

Are these guys Einstein, for figuring out a wormhole between US and India, enough to fool some poor investors? (according to the popular conspiracy theory)

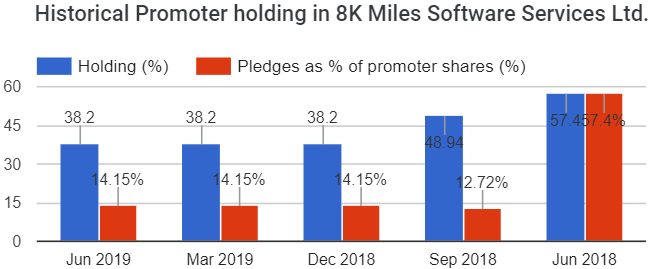

Nothing more has been sold by the Promoter group since December 2018. Somewhat good!

Yes, 20% of overall share-holding has been sold-off since past year. Explains some of the price decline. Keep in mind the pledge has been reduced to only a 3rd of the amount in the same year. Both Good and Bad?

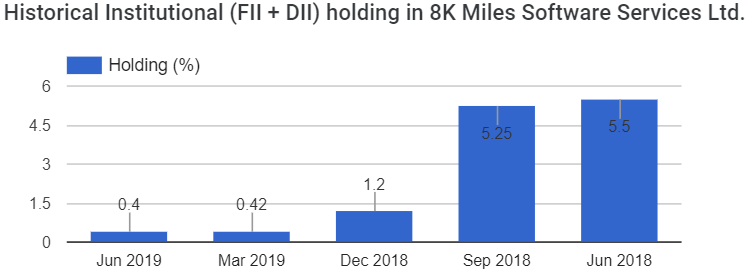

Of course Institutional holdings were marginal and are now almost totally absent

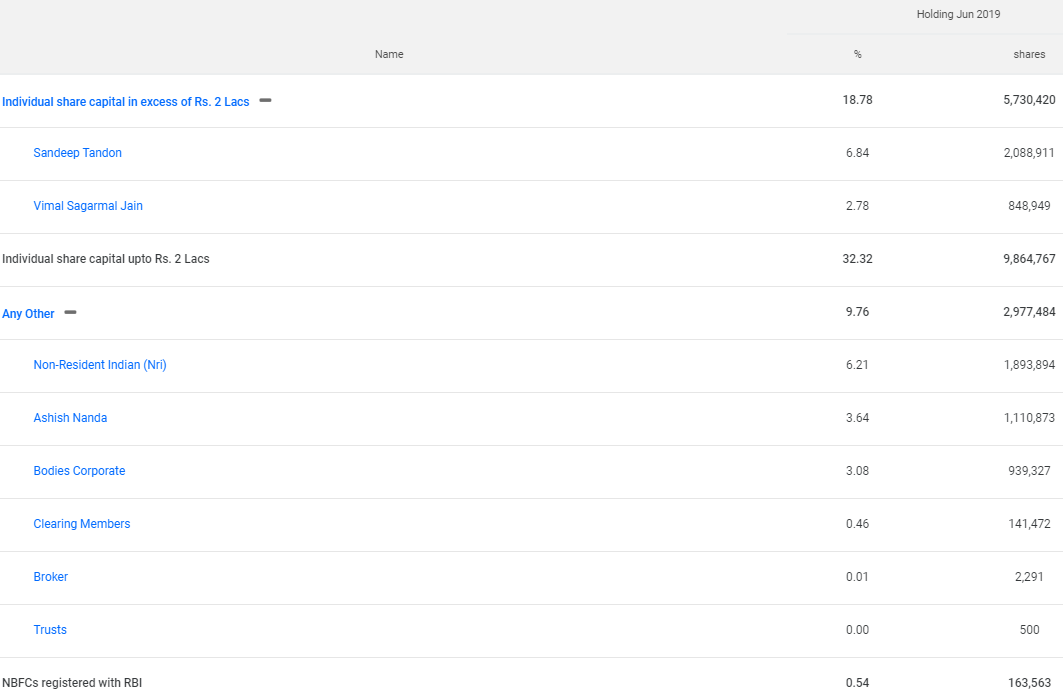

Lots of BIG Individual holdings here: (big ones total 20% of total shares)

SOURCE = Latest Shareholding Pattern - Securekloud Technologies Ltd.

1 Like

So, we do not yet have results for March, full year and quarterly. The board meeting was delayed 3 times:

1st announce

2nd announce (postponement)

3rd announce (actual meeting done)

No results published yet! after 6 months delay.

CFO looks OK

https://www.linkedin.com/in/swasti0665/?originalSubdomain=in

Office looks OK

Linkedin Company page looks OK

https://www.linkedin.com/company/8kmiles-software-services-ltd/

This is nothing but last year’s story repeated all over again.

No further facts added to those already known and discussed here previously!

Thankfully it is now in Z category (NSE/BSE), no speculative day trades, I kind of like it!

The promoters appear to have been “pushing the boundaries” ![]() since the very beginning

since the very beginning

Not serious really, the stock did do well, more than 2x within 3 months of listing. Greed is good? or isn’t it?

This is what a summary shows at the BSE company page:

source = Stock Share Price | Get Quote | BSE

https://www.bseindia.com/xml-data/corpfiling/AttachLive/8c5f614b-4bba-4059-acb5-852351c08f14.pdf

27 SEPT 2019

Sub: Intimation of approval for extension of Annual General Meeting

We hereby inform you that in terms of Section 96 (1) of the Companies Act, 2013, the

Company has requested and obtained approval from Registrar of Companies (ROC) vide its

approval letter dated 27th September, 2019 (attached) for extension of Annual General

Meeting for the Financial year ended March 31, 2019 .

Further, we wish to inform the shareholders that the Company is in the process of completing

the audit and the Annual General Meeting (AGM) will be conducted on or before 30-11-2019

as per the extension given by ROC.

The Company regrets the inconvenience caused and assure these delays will not recur

List includes 8k Miles

2 Likes

NSE as well, from 04 November 2019.

https://www.nseindia.com/content/circulars/CML42373.pdf

Trading will happen on a trade to trade basis once a week for 6 months.

Just remember that this firm was audited by Deloitte and Touche, and its CFO was awarded by the same Deloitte for his work in 8K Miles. They collected fat fees and management piggy backed saying, see, we are audited by Deloitte and by implication they must be true. Trusting shareholders did not know that Deloitte just audited standalone where almost no business happened, and just put together numbers from their US entities.

Promoters sold bulk of their shares at a fat payout, one of them shedding crocodile tears that the broker sold it without his permission.

Many shareholders on this forum too were caught on the wrong foot, and sharing facts to the contrary did not help - probably increased faith in the firm (Backfire effect).

3 Likes

#Krishnaraj

So the company stopped doing analyst meets about 6 qtrs back and that was the first giveaway on the impending crisis.

The US subsidiary has the results of Mar’19 June19, and Sep19 qtrs and FY ending Mar’19 and the investors have no clue what they are like.Being a private unlisted co. in USA it has very little regulatory responsibility.The results and returns must have been filed by the local CPA.

The listed co which is the holding co. will now get delisted and probably sold to some dummy co. of the group so that the US business profits stays with them.The Indian investors will pay for this.

The chief conflict it appears is the US subsidiary which has been declaring inflated profits without writing off the intangible assets and the accumulated goodwill.There are many issues relating to this units accounting and profits and being unlisted and private has escaped scrutiny.With the new listing rules making the statutory auditor responsible for the subsidiary results there has been a face off.

The only consolation is that Harish Ganesan who was the first CTO and co-founder and responsible for the growth during the initial years and thereafter resigned and left has joined back as an advisor and is apparently now based in US.The question now is when will Deloitte announce their resignation.

3 Likes

It has come to my attention with many of the firm’s going bankrupt, the big four are involved in one way or the other.

DHFL and 8k miles are just the tip. Just google how PWC went Scott free in India even in 2019 while it was fined the same year in the US for the Satyam scam.

Bottom-line: unless you trust the promoters, stay away from micro cap stocks audited by the big four if they are shining bright. It’s a warning sign.

2 Likes

No use now but after IL&FS fraud it was required by SEBI etc. that all subsidiaries should be fully audited by the same auditor. Just a standard international rule we adopted now. Ultimately chors are risky. India seems to have a very high number of such frauds/chors.

IIRC, three of the big four firm’s were auditors to IL&FS.

Shady promoters use the lure of big 4 auditors as a way to attract investors and show how they have solid processes etc. So it’s the other way round.

How many firms did the big four voluntarily quit being the auditors for for compliance issues? They definitely have the experience to smell if something is fishy.

The auditors are regularly fined for lapses, ignorance and frauds in the US. Unfortunately, they know how to get away with scam and Commission in India.

Investors smelled a rat in 8k miles much in advance. How come Deloitte missed all the lapses?

1 Like

Board meeting and full results on 2 November

Results declared…

What a stinging audit report by Deloitte.

Mr.Balaji the partner has woken upto the frauds after auditing for over a year and realising how his firm was being taken for a ride.The CEO,the CFO, the US CPA who signed the accounts, the directors all need to be hauled up.

- The auditors state “we came across certain transactions that gave us reason to believe that suspected offences involving fraud have been committed in the Company”.

2)Two “independent directors” who were never independent(one before he was even appointed and the other lost his independence within 60 days of being appointed in 2015) functioned independent directors till early 2019.Every meeting of such directors is void and the consequences…

3)Receivables of Rs30 crs as of 31 Mar’19 for sales - A fake consultancy firm appointed and paid Rs17 crs and no details of services rendered/ownership.Suspected to be a firm owned by the CEO.

5)Rs98 cr investment made by the US subsidiary in privately owned 8K media looks sunk.This subsidiary has to receive Rs33 crs from this private co and the subsidiary in turn has borrowed Rs33 crs from the listed co and looks doubtful if it can repay.

6) Statutory auditors unable to state if the allegation of forgery by the company management has been resolved and not sure if the forensic audit report clearing the allegation is true and correct…

7)Unable to comment on the correctness of revenue recognised and proof of services rendered.

8)Fake sales of Rs24.48 crs and outstanding of Rs34.64 crs.

Shareholders not informed of appointment of a CA firm to verify various inconsistencies in the books of certain subsidiaries.This appointment was made in July 2019 and the report is still awaited.

9)No particulars of services rendered to many customers and te address/websites of such customers are same as that of some employees.

10) Corporate guarantee of US$50 lacs given by listed co to Columbia Bank for borrowings by two step down subsidiaries but no shareholder consent.

In all these, the central player is RS Ramani the ex CFO with the aid of CEO.Money transferred to private cos, fake billing, fake services, fake profits and now the unmasking.

The writing was on the wall for over two years but the investors who could not read the gravity of the situation (revealed substantially in the last two years AR) are the losers.

16 Likes

During March 2017 to March 2018 Ramani offloaded approx 17 Lakhs share during the peak share price of 8k mile. If we conservatively calculate the price it will be more that 100 Crores! Is there any possibility of related party transaction between core position holders?

The report of the auditors is stinging, and gives us a good idea of the playbook used by the Promoters to suck money out.

Deloitte needs also to answer why did they not unearth this for FY 18, that would have brought this fraud to light much earlier, and prevented substantial siphoning in FY 18/19. Deloitte’s name was used substantially by the CEO to say that the firm’s accounts were credible. In fact the CEO paraded them in the FY 18 AGM.

I think many retail shareholders (including members here) got badly stung, and in some cases as can be from the older posts above, even analytic evidence pointing to fraud was dismissed by them. On the flip side we get opportunities to learn very important lessons:

-

The most important lesson is the one that Ben Graham laid out about 70 years ago ‘Obvious prospects for physical growth in a business do not translate into obvious profits for investors’. Cloud was seen to be a very very big opportunity and it was even more obvious to retail investors working in the IT industry. So obvious and opportunistic that it blinded them to other factors that are essential but not obvious to translate that opportunity into profits for shareholders. In fact the competitors that the CEO himself pointed out to - Cloud Era, was itself huge losses compared to the wonderful margin shown by 8K. But highly enamoured investors said that CEO’s comparison was wrong implying that they had a better understanding of the industry to explain 8K’s wonderful margins. I had a similar experience myself when I was enamoured of Internet stocks back in 2000, and was running an Internet based business.

-

Substituting the anecdotal for the statistical. What we hear, see and feel arouses such excitement it overtakes the cold and unemotional numbers. If I work in the industry where I continuously see some cloud deal or the other, I read reports all over about cloud, I live in a professional environment where my colleagues feel the same, I will automatically (System 1 of Kahneman) believe 8K’s story to such a degree that I will discard numbers and what it reveals. Similar to people decoding India’s GDP growth just by looking at what’s happening around them - so overwhelming that the stats get dimmed out. But the reality is that ‘in the long run mathematics trumps psychology’.

-

Avoiding disconfirming evidence, when one must do exactly the opposite. Whenever we buy a stock we have a thesis on why we are buying it. But subsequent to our purchase, we always look at evidence that confirms the thesis rather than disconfirms it. We should however be doing the exact opposite looking for what will upend our thesis so that we can immediately know if our thesis is wrong. Since those selling the stock to us will do the exact opposite - they will give only confirming evidence on why we need to be buying the stock, we are unsure, thus we tend to look for confirming evidence.

-

Knowing and keeping in mind the incentives of various players when evaluating. In a capitalist society everyone has incentives and most people succumb to incentives to the exclusion of what is true. If we are not aware of the incentives or if we are not taking it into account, we will end up beguling ourselves. For instance it becomes clear now why the CEO said the CFO sold shares ‘because he had a charitable commitment’ (dump the pumped stocks), why Deloitte gave an award to this fraud CFO for ‘silently working behind the scenes’ (collect fat fees) and now doing an about turn (harmed reputation), and so on.

Cheers,

17 Likes

Manpasand is still trading but 8K miles is off both BSE and NSE.

Are these criminal offences?

Promoter holding is frozen by SEBI. Can this be taken over like Satyam?

Disc: exited a month ago.

I learnt a lot about behavioral investing from this very thread, having participated a lot in bringing out and discussing the negatives. I noticed an unfortunate thing in the process - instead of being open to disconfirming evidence, apart from the expected ad hominem, it appeared to make the conviction of the holders stronger, because the will to prove oneself right becomes stronger than the will to protect one’s own capital. Its the bizarrest thing.

Now that the auditor has alluded to the books being cooked - inconsistencies in bank statements, particulars of services rendered missing in transactions, inconsistencies in names of Customers, fabricated communications with vendors, inconsistencies in Customer addresses where sometimes addresses used belonged to the employees - the list is long. The pump and dump, as well as siphoning, everything alleged here in the last couple of years have all been acknowledged. It is a relief that the truth is finally out.

All the losses and crosses are borne solely by the shareholders. After all the misleading, everyone from the promoter, auditor, CNBC which repeatedly gave time to a crook to cause further damage will all go scot-free for a rinse and repeat. I hope the ex-shareholders here aren’t lathering the next one.

31 Likes

#diffsoft

The most scathing comment of Deloitte which I hardly get to see in other audit reports is what they say in the report-“in view of matters reported in paras 4 to 10 above, and in the absence of reliable cash flow projections by the management…we are unable to comment on the appropriateness of the going concern assumption by the management…”

This means the company doesn’t have resources to survive for long and has been bled by Ramani and Suresh.

Also the auditors say they were not allowed access to the books of their UAE subsidiary.

Coming to your accusation of Deloitte rewarding the CFO two years back, in the past I have seen E&Y do the same.These rewards are based on quid pro quo and one of the winners of E&Y emerging entrepreneur who went bust one year after getting the reward told me how he became the winner.

Last year the auditor did comment on the share sale by the promoter and also reversed some of the intangible assets.Could they have done more?Looks difficult, given the short tenure.

As I understand the statutory auditor had to take the figures of the subsidiary provided by the management and could not review the subsidiary accounts

Some of the comments speak volumes about corporate governance which was audited by the local auditor.SEBI having realised how this loop hole was being exploited amended the LODR rules beginning Apr.19.

Some of the notes speaks volumes about the corporate governance and how the management ganged up to cheat the investors.See the rep[lies of the management to the qualifications.Nothing but contempt.

Having met Suresh over the last few years I always told him his accounts were suspect and last year when I told him about his “intangible asset” being used to boost EBIDTA he didn’t deny it but asked me how he can redraw the books.

This company will now go the DHFL way with more revelations, enquiries, notices,raids and shareholders may never get an exit.strong text

4 Likes

Yes, awards are worthless, I keep getting repeated mails from CIO review etc. various magazines which look of considerable repute, of making such deals. Advertising space, promotional (paid) content/articles for awards, such as “top 10 cloud provider”, “amazing IoT companies list”. My company is defunct BTW, has been for many years now and was at best a body shopping/pure HR concern. We have zero IT knowledge/work, ever.

PS: I do hope SEBI makes sure these people get the loving they deserve, in jail.

3 Likes