Going through the annual report.

Travelling and Business Promotion expenses : ~19 Cr in the last year. Out of 120 Cr revenue, 19 Cr for business promotion and travelling sounds like too much.

Is there a way to find out the number of employees employed by them?

Is the business model related to headcount like other IT services vendors? They mention a lot of frameworks that they use - It sounds like the model is linked to IP and consulting rather than headcount - Would like to know more.

There is no mention of recurring revenue from existing clients like other IT vendors publish - No breakup of Fixed versus Time/Material

Their Cashflow statement is a bit difficult to understand and needs more study.

Intangible assets mentioned sound like Goodwill from acquisitions rather than the assets like IP frameworks they have built/acquired - Entire amount of intangible assets are goodwill? Could not find breakup.

I’m trying to understand the exact same thing. How can a company that has given a minimum of 100% growth in revenue over the last 8 quarters and 100-200% growth in net profits in the same period trading at a trailing PE of less than 18x now. This is assuming 0 growth in the coming quarters (Sept quarter’s profit is at 23.6 crores, therefore full year’s profit’s at 100 crores). With a 20% growth in NP QoQ (they’ve been growing at a faster clip than this if take the last 10 quarters) for the coming quarters this should be close to 130 crores for the full year which makes this even cheaper @ 14x and falling even faster in the coming years.

In fact, with the demonetisation move coming in recently and the rupee falling further (besides the bumper results this quarter), I expected this stock to have been one of the few resilient ones to have been able to withstand the market crash but it seems to be falling faster than other stocks that will have a significant impact on their earnings growth in the coming quarters. I don’t see 8k Miles being affected in the coming quarters due to the demonetisation move as their business largely comes from the US and a few other countries. In fact, I can see some tailwind from the fall in the rupee.

Has anybody been able to understand the market’s reaction to the stock over the last couple of weeks?

Disclosure: Forms 6% of my portfolio. Added some during the recent market correction and looking to add more at the current price.

Edit: https://yourstory.com/2015/07/obamacare-8k-miles/

Could Trump’s (and hence the wiping out/partial repealing of ObamaCare) victory possibly be the reason for the correction in the stock price? Wonder how much of an impact that would have on 8k Miles. Views invited.

If market is dumping because of Obamacare repeal or trump win, that might be an opportunity to buy - Its very hard to predict how these things would pan out in the longer term.

I sent a mail to their investor department asking for breakup of rev numbers by work location, old vs new customers - Did not get any response. has anyone been successful in getting a response from them?

Probably because they are trying to raise the capital worth 500 cr which will significantly dilute their equity…so once they will raise the capital probably overhang will dissappear and then market will decide future course…

Hi guys…remember ppl got more split shares and also a bonus just a month

back…they may sell some…isn’t it an opportunity for someone wanting to

buy more…

8k Miles has been recently covered in Ambit’s forensic accounting report. They have used “Thousands of Miles” name for the company on page 38. The report highlights some serious red flags on corporate governance and aggressive accounting.

The report has highlighted the difference in summation of net profit and cash flow from operation. As per the data from screener.in the summation of cash flow from operation over 2011-16 is 57.5 cr whereas summation of net profit for the same period is 74cr.

I believe this difference is normal and generally seen in fast growing, small companies. This data need to be supplemented with additional information to deduce that company is in any way tinkering with the financial information.

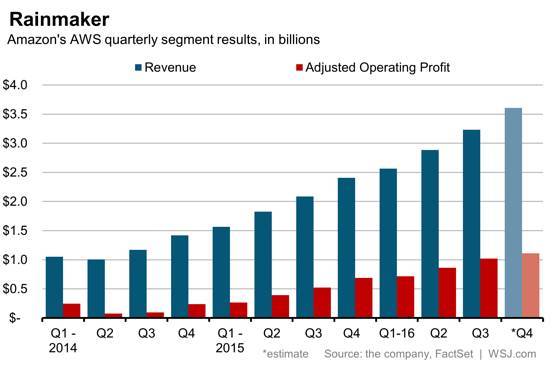

As far my check goes company is a highly regarded in cloud and is featured on the websites of Amazon web services and Microsoft Azure.

The all new AWS managed services forces important buyer and partner decisions

By Kurt Marko

December 16, 2016

Earlier this week, AWS declared that it is entering the managed services business with an offering designed to bootstrap cloud adoption among the largest organizations.

The company says it has been working on the service for the past couple years with select enterprise customers and partners helping it to build a service that simplifies deployments, migration and ongoing management using a new set of automation tools and APIs.

Although the new AWS Managed Services (MS) makes perfect sense given the complexity faced by large organizations migrating application and data to the cloud, it seems to duplicate offerings already provided by AWS’s stable of managed service partners such as 2nd Watch, 8kMiles and Accenture.

Source: Diginomica.com

Though at the outset the above news seems unfavorable to 8K Miles, opposite is true as well.

AWS entry signifies the market potential and growth prospects. Amazon competes with its ecosystem partners in very few areas (like video, this etc,) and their entry signifies the importance Amazon is according to this space.

AWS entry will standardize the offering and will bring significant consistency in service delivery, governance, management and monitoring. This will increase the awareness and market size and all the partners will stand to benefit.

AWS will be expensive. When standards based offerings proliferate, the lower cost providers will stand to gain over the medium term.

AWS offerings will raise the bar. Will help 8K Miles and the likes to move up the value chain.

I agree with you that it will standardize the offering. Amazon business runs on scale. This is how they are able to provide AWS service at low cost. I wonder whether 8k will be able to compete Amazon in pricing in long run (w.r.t AWS MS once it gets standardized). Also, why would anyone associate with 8k if Amazon itself provides the transition. Amazon currently need partners to grow its AWS offerings. But once it gets the traction Amazon will try to bridge the gap between itself and end customer where ever it can. (Amazon is a customer centric company, they don’t like intermediaries)

Has anybody been able to wrap their head around why this stock is stuck at these prices for the last 1.5 years? For a company posting such scorching growth quarter after quarter, year after year, in a sector that’s expected to grow manifold over the next 5-10 years, having big clients in their pocket to show for, being recognised as a “prime” partner with Amazon and now recently getting covered on Forbes. Can anybody throw some light on why they think this is the case and also what they’ve made of the “revelation” of Ambit Capital’s coverage of 8k Miles (exposing them so to speak)?

Company’s balance sheet is not perfect. for a total balance sheet size of approximately 500 cr, 175 Cr is intangibles like goodwill and product under development, receivables and other current assets at 200 Cr. So out of 500 Cr, 375 cr is questionable. Only non-questionable item is cash which is 90 cr. But they also have a short and long term debt of 27 Cr. Generally, I stay away from companies that have both huge cash and debt. there may be some genuine reason for carrying debt when you are sitting on a ton of cash but other items like receivables and goodwill is a turn off.

Cloud is a highly capital intensive business so I would expect they would carry lot of hard assets and clients should pay quickly because they cannot afford not to.

While Cloud infrastructure providers like Amazon will have hard assets which is capital intensive. Cloud service providers like 8K Miles does not carry hard assets.