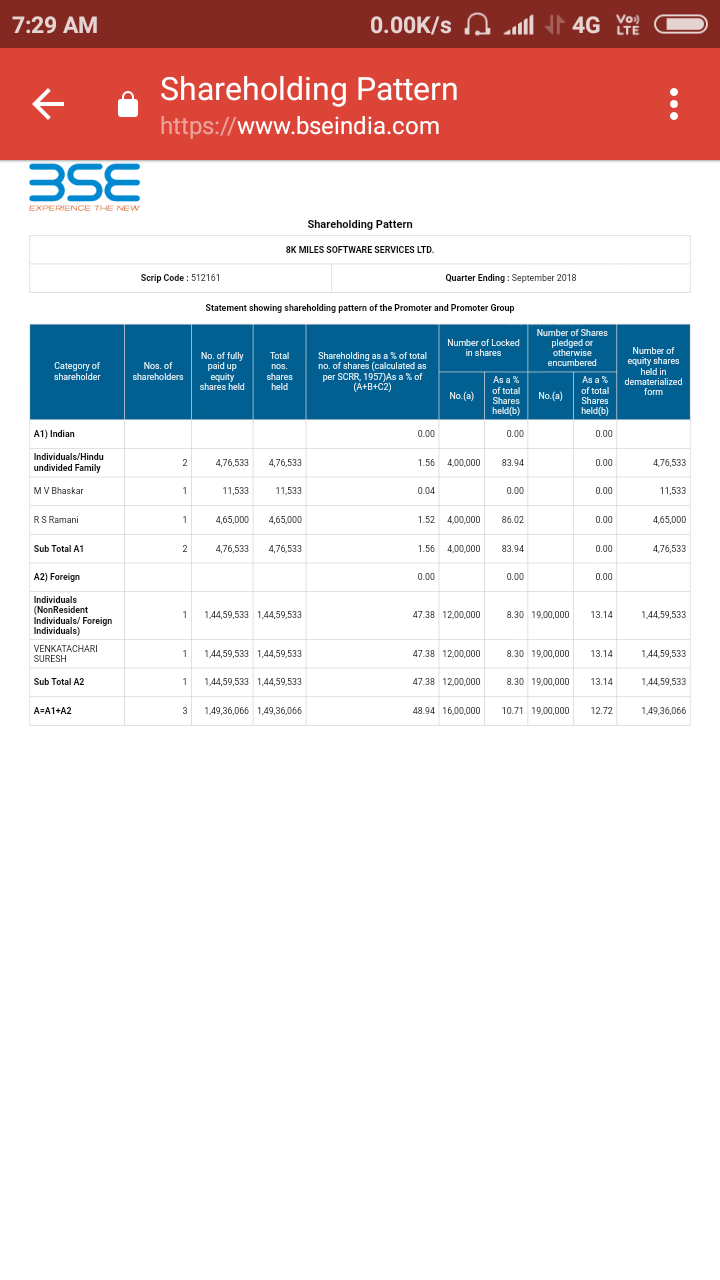

Thanks for sharing the SHP, in fact Sandeep Tandon’s holding has gone up (I don’t know why it does not show up in SAST).

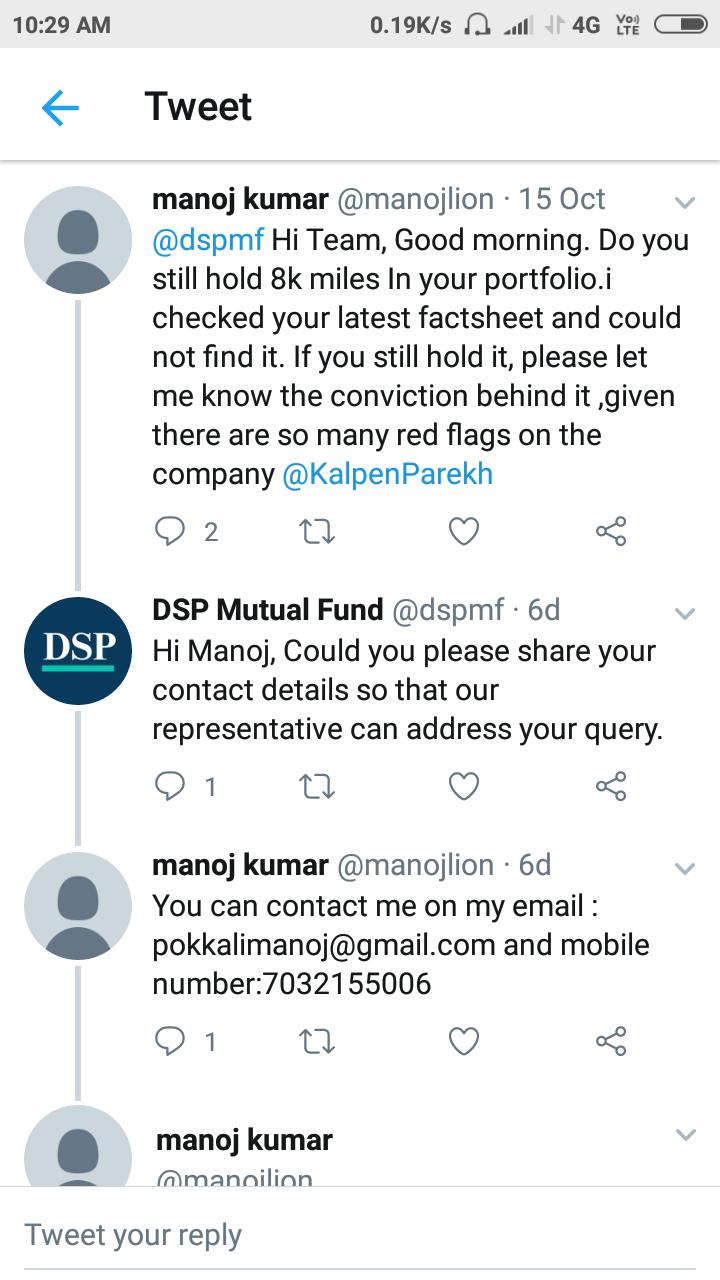

There is however an additional sale of 25,00,000 shares sold by SV and debited from his demat account on Oct 1 as per the Insider Trading data. This is over and above the 25,70,000 of his shares that he says were done without his consent / knowledge.

These shares were ‘disposed’ for ~ Rs 48.1 crores and at a price of Rs 192.25. This price was the price in BSE as of Sept 28. Thus his stake would have been reduced further by 8.19%.

The source for this information is this link - with fields filled in as ‘8K MILES SOFTWARE SERVICES LTD’ for the Security Name and beginning and end dates as 01 Jan 2018 and Oct 21, 2018 respectively.

The corresponding CSV file is shared here BSE InsideTrading722102018 8K Miles.xlsx (11.5 KB)

(saved as Excel Workbook as VP does not allow upload of CSV files). If you filter for SV and net off acquisitions and disposals you will find the following (I have put a minus sign for acquisitions):

Net total shares debited (by way of net of Disposals and Acquisitions) from 20 March 2018 until 11 July 2018: 25,70,000.

This matches with SV’s claim that 25,70,000 shares were ‘illegally’ sold by the brokers and refuted by atleast one broker

Total shares debited (by way of net of Disposals and Acquisitions) on 01 Oct 2018: 25,00,000.

So it seems shares over and above the claimed 25,70,000 were sold at the price on Sept 28 (it hit lc then) and debited on Oct 1, 2018. This should reflect in OND SHP, unless similar numbers are acquired.

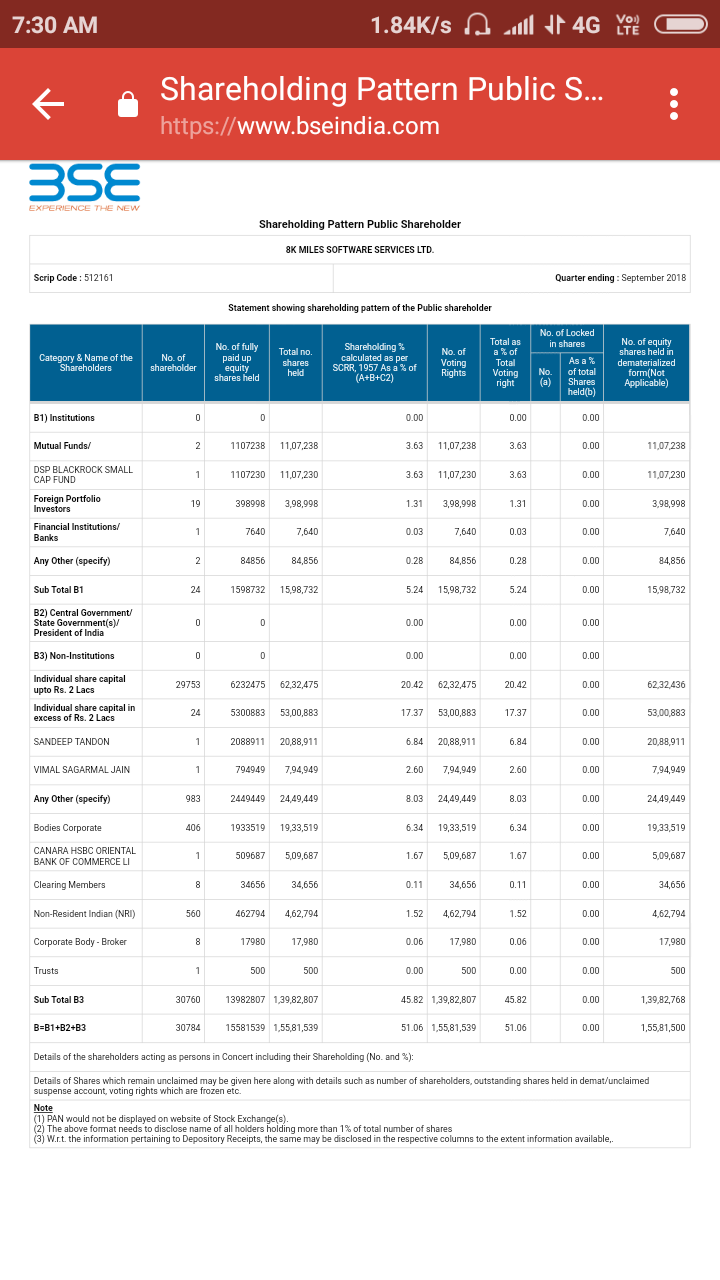

From the trades and the Sept 30 SHP, bulk of the buyers were Individuals less than Rs 2 lakhs. So it appears that the ‘illegally’ invoked shares were hitting the market from the Sell side. And if an additional 25,00,000 have been ‘disposed’, it seems to me there’s much more to come.