My two cents as an industry insider. Market size is huge around $200B by 2020. Big 4 will surely play in this area, but don’t think it can make a HUGE difference to their large mcaps, but small & serious players like 8k, Cambridge, Persistent will surely make big gains. It is all about sector tailwind.

All big IT companies are already heavily into this.Being a partner with product vendor is good but don’t think it can be considered as MOAT.

https://aws.amazon.com/partners/msp/

Atleast 30+ partners are already listed including Infy/Wipro and Cognizant and this list will only grow.

Amazon is the product vendor and 8K miles are managing the services etc. for amazon cloud, as per my understanding they are simply a product partner in a fast growing area (Almost all Product companies have tie ups with implementation partners for their products).

The opportunity size is definitely huge and focused players will grow fast in this area,however personally 90-100 PE is way above my comfort zone for this kind of company.

Disc-Not invested

2 Likes

does this company provide any other value-add beyond bringing a customer to amazon/Microsoft cloud? i.e while implementation can be done by any partner of Amazon/MS…what does it have further to offer(like Big Data Management , its Analysis softwares…)which will help/ensure customers stick for longer term or attract new customers to it vs established players? also…like it bought a company to provide USFDA compliance services…is that a niche area not serviced by others?

1 Like

Hi Amit,

What cld be the key differentiator for 8k miles or Persistent. Persistent, after reading the ARs, I have understood that they are into Product development and help in enterprises transform into digital, besides the platform and product strategy. Can this not be done by others? Others either have low ROE, or do not pay dividends etc.

I do not have an IT background, hence the query.

Disc: Not invested in any SMAC company.

Great Q3 results.

8K Miles Q3 , revenue rises 114% , EPS up 93%

It has got a moat and has patented services. Thereby ensuring monopoly kind of business in niche area. Long way to go, as the sector itself is growing fast. The next opportunity is cloud banking. BFSI

First post in this forum. I invest in tech companies (private) and have been watching the 8k miles story with some interest for a while now. Few points

Positive

- The growth is real and there are enough tailwinds to continue 50%+ growth for the next 2 years

- As more companies move to cloud (instead of building expensive data centers internally), the market size will only grow. Amazon is the clear market leader and 8k Miles has a fantastic first mover advantage when it comes to it Amazon alignment

- While its true that there is no moat, there is a segmentation issue here. Infy or Wipro will never bid for or implement sub $1m or eveb sub $5m contracts. Most cloud computing implementation contracts are sub $1m or even sub $500k, which are too small to make sense for a large IT services player or even a mid size one like Mindtree.

- In the unlisted space, players like Happiest Minds, have scaled to $50m RR in less than 5 years by delivering the same set of solutions

The downside

- There are no recurring revenues in this business. You implement the cloud offering to Amazon and that’s it. There is very little or no maintenance work. What this means is that while it is easy to scale to a 300-400 cr revenue business, you can’t really build a 1000 crore business without recurring revenues. IT services success stories have been built by converting projects into long term engagements, converting a $1m client to $5m and then $10m and so on. It is unclear as to how 8k Miles will do that. A good example would be to see how a whole bunch of SAP implementation players fell by the way side. I suspect 8k miles doesn’t have much more runway beyond a 500 crore run rate (from the current 300 crore run rate).

- This is a strictly linear IT services model where costs will rise in proportion to revenues, there is very little margin expansion potential

- Valuations, well, make no sense even after adjusting for 100% growth. Currently business has a 44 crore PAT run rate and a 300 crore revenue run rate (Dec qtr *4) . At 2700 crore market cap it trades at 9x RR revenues which is ridiculous for a services business that has no recurring revenues (like SaaS / product businesses). You will see this taper down to 4x-5x very soon (no one knows when) which will end up in keeping the market cap flat even if the revenues double to 600 crores.

- I have always been unclear about the origins of the company given the promoter’s history. There are a bunch of insider trading cases http://www.business-standard.com/article/pti-stories/sebi-rejects-erstwhile-promoter-s-plea-to-sell-8kmiles-scrips-115032400760_1.html

I would be wary at entering in this price, but frankly I have been vary since it was 1000 and I have been wrong. The markets can remain irrational for longer than you can remain solvent!

16 Likes

Thanks for the input. However, I am not sure about your claim of “no recurring revenues” in this business. I am not aware of this business and request IT people to throw some light on this.

The company essentially helps customers migrate to AWS through a 3-6 month project. If you had a small retail chain and wanted to migrate to AWS, 8k Miles would send consultants over to implement that change (migrate data, set up servers, storage, email etc) and charge you a fixed fee of say $200k. In fact if you look at Company’s financials, they report revenues as “Project revenues”.

Think of them as an EPC company instead of a BOT company. It is very different from a BOT company in terms of revenue stickiness and recurring nature. It’s an orderbook business which has a limited scalability. I have not heard anything from the management yet on how they are solving this problem. You can get to 300 crores of revenues with 50-60 projects but to get to 1000 crores of revenues you’ll need 200+ projects which are very tough to manage and win.

Hope that makes sense

5 Likes

Thanks for clarifying. It really helped me to understand the nature of business.

Thanks for the insight! The issue is we might be underestimating the longevity of this business. Let’s go back to late 90s and everyone thought that IT boom will get over after Y2K implementations. Well the rest is history. I just think the opportunities might keep coming in terms of analytics, change in business parameters etc etc just like they did over the last 15 yrs. We might not be to equipped to imagine everything right away. If the management is competent, things will keep falling in place.

Disc: No holding here but invested in Cambridge and Kellton

2 Likes

Thanks. That’s right in this space it looks like there is a lot of growing opportunity like you said. Internet of things is a huge opportunity in next 5 years.

Disc: I am not invested and not planning to considering the crazy run up and lack of risk reward.

But came across below research report which highlighted the future focus of mgmt into Life-sciences segment.

http://research.adityatrading.com/Reports/CR06112015061311.pdf

Healthy acquisitions in Healthcare and Pharma Sector to gain more market share of Cloud in Pharma Sector

8K Miles over the past 12 months has acquired three firms in the health and pharma space. Earlier this year, it had acquired the US-based Cintel Systems, Canada-based Mindprint and another US-based firm SERJ Solutions to strengthen its portfolio in the fast-growing life sciences sector. It also acquired US-based NexAge Technologies, that specializes in the life sciences sector last quarter.

Cintel Systems is a user interface (UI) and user experience (UX) design and development services company. The deal size is $3.75 million and is a combination of cash and stock. The acquisition expands the mobile competency of the company’s cloud offering and helps it gain access to Cintel’s enterprise clients and add over 70 Mobile, UI & UX experts in the US

Mindprint is a clinical research software startup focused on analytics and operational software for Clinical Research Organizations (CROs) and Pharmaceutical Sponsors. The acquisition involved $150,000 in cash and $250,000 in stock.

Company said - Mindprint domain knowledge of clinical research and pharma outsourcing operations will provide 8K Miles additional competitive advantage to capitalize on the growth potential in the related markets in India and abroad.

SERJ Solutions is a provider of innovative Epic EHR consulting, custom application development, and support solutions for the healthcare market.

―By taking advantage of our expertise in cloud technology and information security, and combining that with deep healthcare domain expertise, this acquisition will allow us to create a compelling suite of cost effective hosted SaaS solutions that healthcare providers can deploy," said Suresh Venkatachari, chairman and CEO of the company.

NexAge Technologies USA Inc. is one of the principal regulatory compliance and technology solutions company in the U.S. with more than 15 years of experience in Computer Systems Validation, Quality Review, Vendor Audits, Data Analysis and Migration, Analytics, Change Management, as well as Governance for the Life Science and Pharmaceutical industry. The total consideration in cash and stock, for the acquisition is $3,000,000 dollars ($1,500,000 in cash and $1,500,000 worth of US subsidiary stock).

This acquisition will boost company’s world class CloudEzRx™ solution that has been designed with an ultimate goal to address qualification and validation compliance for applications running on the cloud securely with the larger purpose of empowering Pharmaceutical and Life Sciences enterprises to utilize cloud services across value and supply chains.

Further company said growth could be through both organic or inorganic routes meaning in future too 8K will seek healthcare, lifescience and pharma sectors as the company sees strong opportunity in the cloud market, which is getting matured.

Government policies to boost demand for Cloud and IoT

The recent Supreme Court order legalizing Obamacare across the US is a big boost to cloud players like 8K Miles.

ObamaCare is a US healthcare reform law that expands and improves access to care and curbs spending through regulations and taxes.

The health law, which will bring millions of uninsured Americans health benefits will be a critical boon to pharmaceutical industry balance sheets, increasing revenue by one-third by the end of the decade, according to a report from research and consulting firm GlobalData of London. That means the U.S. pharmaceutical industry’s market value will mushroom by 33 percent to $476 billion in 2020 from $359 billion last year.

The Life Sciences Industry in the US is currently facing tough IT challenges driven by a need to create more innovative solutions within shrinking IT budgets which makes it even more important to design agile cloud centric solutions and business models that are rapidly scalable. 8K Miles CloudEzRx™ framework enables customers run critical workloads securely on the cloud and is designed to meet security, analytical and operational needs while addressing the unique regulatory compliance requirements faced by Pharmaceutical and Life Sciences companies. The domain expertise of 8K and proprietary IT solutions in data migration and analytics will enhance and further improve the overall portfolio of its solutions targeted to the Life Sciences industry.

Through this acquisition, 8K Miles gains access to the network of Enterprise customers and strategic partners acquired by NexAge during the last decade.

My perspective from Phama pov:

- With increasing usage of wearables and bio-sensors (IoT), there will be data deluge from clinical trials which will need heavy duty processing. There would be a drive towards cost-effective scalable cloud platforms.

- Same would be the case with complex biologics molecules which involves gene-editing, genome sequencing, immunotherapies, etc.

- AMC for life-sciences segment could be a source of recurring revenues.

2 Likes

Not underestimating the market potential, but my fundamental question is with the business model and the crazy valuation . What people forget about the IT boom is that only 4-5 of the 100s of IT services players have scaled. The rest have disappeared or continue to wallow at single digit P/E multiples.

Even if 8k miles does really well , The current valuation of 9x RR revenues will inevitably readjust to 3-4x RR revenues since growth % will slow down (larger base of revenue) and hopefully stock liquidity will improve.

Current market cap is 2700 crores and RR revenues is 300 crores.

So even if RR revenues doubles to 600 crores and multiple drops to 4x then your market cap will stay at 2400 crores.

For you to double your money (i.e double the market cap), then 8K miles needs to have a mcap of 5400 crores which will require them to have 1350-1500 crores of RR revenues at 4x RR revenue multiple (i.e 350-400 crores revenues in a quarter up from 75 crores right now)

The risk reward proposition now is too skewed in favour of risk. Your best case scenario at current valuation is a 2x over next 4-5 years. Worst case scenario is a 40-50% drop given slowdown in revenue run rate and the subsequent drop in valuations

8k miles is among the most expensive IT services stocks in the market now. I prefer Kellton tech to this because at 300 crores Kellton trades at less than 1x revenues. Downside is low there.

![]()

![]()

1 Like

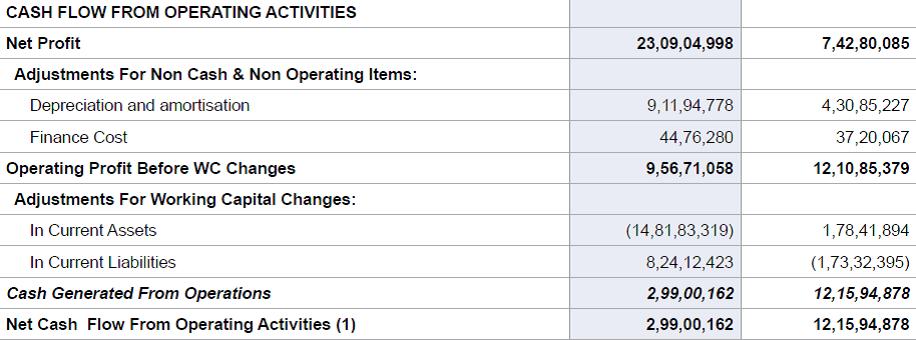

The accounting information given in the AR for this company is a joke. Basic number don’t add up. Just as an example look at the cash flow from operations.

NP + Depreciation + Finance cost - WC capital changes should equal Cash flow from operations. Which adds up for FY14.

( 7.4 + 4.3 + 0.3 +(1.7-1.7) ) = 12.1

But look at FY15 numbers. They make no sense at all

23 + 9.1 + 0.4 + ( -14.8 + 8.2) = 25.9

But number given for cash flow for operations is 2.9

This is just one example. The whole AR is full of such cryptic numbers which made no sense to me at least.

4 Likes

One of my friend, who is Sr VP with a mutual fund house warned me of serious accounting issues in 8K Miles’ and Cambridge. He also pointed finger on auditors. Since it was way off my comfort zone, I never dug further, but above post reminded me of that discussion.

1 Like

All three stocks (8k, Cambridge and Kellton) had management change and were kind of penny stocks before that. They were expected to clean up books post management change. I did not find any major put offs in Cambridge and Kellton’s Fy15 ARs but the above example raises questions about 8K. I did find other issues here and there are stock manipulation allegations against previous managements of Cambridge and 8K Miles. I have high regard for Cambridge’s current leadership and that’s what attracted me. Surely one needs to be cautious and convinced before putting some money here.

1 Like

Very rational doubts, which exactly made me to sell my stock recently @2310. However i don’t see those buying at this price as irrational fools!

The company is doubling the revenue annually since the last year! If it makes a revenue @ 1200 in next 4 years(4 times the present revenue) , it can gain a EPS of 150 which makes the present price 15 times multiple (PE 15). So for a company gorwing at a break neck pace of 70% revenue growth with 0 debt and PE of 30 is acceptable , that makes the fair value of 4500 in next 4 years. That is 100% return with CAGR of 25% …

For this scenario to work out the company needs to make its revenue 300-600 and then 900-1200 in next 4 years. 1 or 2 acquisitions will give this number significant push (discount the profitability though, but that should be negated again by the synergy in place). So for risk takers 2250 is not at all bad price.

But But , we need to discount the the uncertainty which skews the ratio more towards risk rather than reward. Main concerns being world economic volatility,management execution capabilities, one failed acquisition , any of these will throw the growth story into toss. That’s why i did exit from this recently.

In addition the AR has plenty of notes to watch , although i did not go through it in details, it is kind of surprising that company can go wrong so pathetically in numbers!!! Elementary CA stuff!

1 Like

Aashish Kalra, chairman of Cambridge Technology Enterprises (CTE), is back in India and this time around he comes with a $12.5-million innovation fund for the big data and analytics industry.

Aashish Kalra in an interview to VCCircle https://www.youtube.com/watch?v=-Qs9p8MaXWg

1 Like

friends,

any one tracking ramco systems ltd.its a cloud enterprise software company,focussing on providing faceted enterprising softwarein the verticals of hcm(human capital management),erp(enterprise resource planning), and m&e (monitoring and evaluation for defence and civil aviation)

recently came across and shall add more inputs as i gather so, going forward.

i invite opinions, study of fellow members.