I don’t know how significantly you folks tend to treat the Beneish M score, but it has been signalling possible earnings manipulation for the past 4 years. For good businesses, free cash flow also reflects reported net earnings proportionately. The lack of this doesn’t look like a good enough sign to me. As a result, I’m not guaranteed of the first tenet of investing: preservation of capital.

I agree with your view points, due to severe drop in midcaps stocks, we have become more cautious and see things negatively. Even a slight underperformance and stock is crashed. I did analyse results. Most part I liked most is AMC revenue is growing in total revenue which will give stablity in revenue projections and help company grow. If Deloitte has audited results that too for US based operations than profit coming is for real. Market is apprehansive for receivables. Things will normalize with time. Don’t find any issue, invested at lower levels.

I don’t understand one thing. If stock is so cheap (4-5 PE) , market cap of 800 crores on profits of 150-200 crores approx , and business is v good. Why the promoters themselves don’t buy the stock from open market. We may find no.s doubtful but they knows the truth. Than what is stopping them to buy from open market , if no.s are genuine ?

Yeah , but they can buy in their personal capacity also from open markets , if business is intact , fast growing and have no real issues in fundamentals. If I was the company owner with insider info and if their were no issues , I would have bought heavily at these prices from open markets. Why don’t they ?

I was looking into this company and the reason why it fell so much

A stock hardly falls due to retail investor action

There are some bulk deals

I have few reservations so didn’t look much into 8k miles

Firstly their profit growth comes from buying companies and integrating them

The large increase in intangible asset is due to recognition of goodwill, any accountant will tell you there is nothing wrong in that treatment

My worry is that the company is trading at a small profit multiple. Buying anything is expensive. When you have a high multiple, buying cheap companies makes sense.

Just because profit is increasing is not a good thing.

As someone said Pe is not everything. You can buy a business that has 10 year software contract and the extra profit from that contract will increase the profit and decrease the Pe

The cost of acquiring becomes goodwill and intangible asset. The management has been doing this sort of growth of profit

Second thing I didn’t like is if the Pe is so Low, instead of buying competitors, why don’t they buy their own stock as it represents better value for company funds. It is also a way of increasing eps and hence indirectly the Pe

On cash flow analysis, I don’t think the management is dishonest on financial presentation. I haven’t checked in a lot detail but had a cursory look and it looked fine

I think the stock has to fall to reflect writeoff of entire goodwill from profits. In software business this is really very short life. Who remembers compaq computers whom hp bought? I think last quarter profit times X 4 X 10years - goodwill should really be the market cap of the company

Divide by number of shares, that should be the sp

This company has never given dividends so the resulting sp I would discount another 30pc to arrive at a price I am comfortable to buy

No. of shares sold by KOTAK MAHINDRA INVESTMENTS LIMITED on 3rd July (the day when it fell from 390 to 300) was 1.7 lakhs. But the total number of shares traded on that day was 66.5 lakhs. Do the math. To me, it looks like the fall was due to retail investors action. Patient investors seemed to have lost confidence in the company. Even one of the active investors on this thread quit on that day. Also, on the day when it fell from 500 to 390 (July 2nd), there was no bulk deal. The fall was due to retail investors losing confidence/panicking.

No, goodwill remained almost the same in the last 1 year. It’s the other intangible assets that went up from 6cr to 225cr.

Buying anything is expensive? What do you mean by that? What if the company has bought something lesser than book value? Is that expensive too?

NO. The cost of acquiring something above book value will become goodwill.

Buying own company shares will benefit the shareholders and will improve metrics like P/E, ROA, ROE. Buyback is nothing but returning cash to the shareholders. There may be opportunity costs. What if there can be better use of that cash? Company knows better than us, retail investors. Also, share repurchase is only an artificial lift to the EPS, when there is no real growth in the topline. I’m in no way defending the company, but just giving a valid reason why the company is not repurchasing shares. But repurchasing will boost the confidence of people who doubt whether the cash is real.

Goodwill has to be written off only when the value of the acquired company/asset falls below the amount for which it was acquired. As long as the acquired company generates enough income and cashflow, why would the company write down the goodwill?

Disc: Staying 8k miles away

I have not checked much in detail but buying any company is not cheap when your own pe is low

It’s simple maths

If you are buying a company for 10x profit whereas your market values you at 6x profit, you are making a loss. Unless you are enjoying a double digit Pe in upper 30s and over, any buying is ludicrous!

Just intangible went up without goodwill ! Wow

I didn’t see that, as I said, I didn’t go into a lot of detail

Goodwill writeoff, is on impairment, you can take a prudent call but in case like compaq computers, whatever goodwill was in purchase got impaired within a year. It’s one of those things that auditors can be convinced, is still not impaired

But if goodwill hasn’t changed

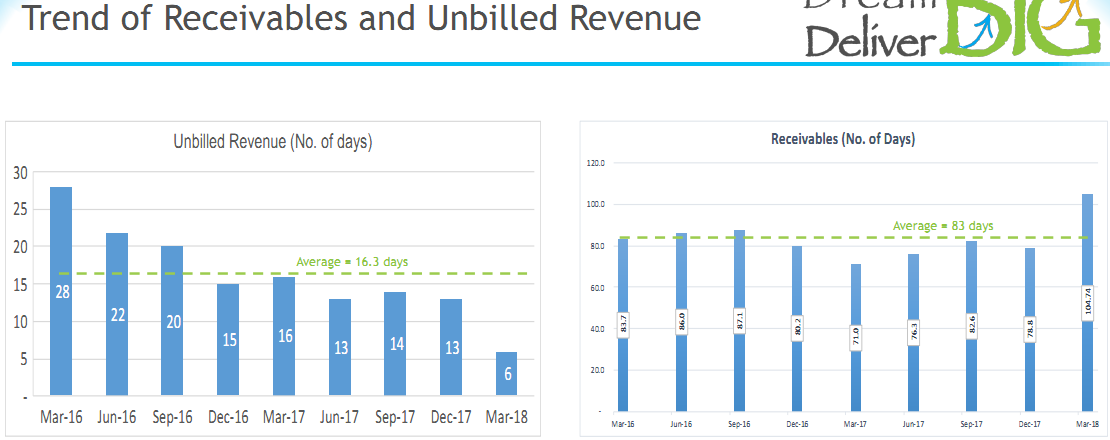

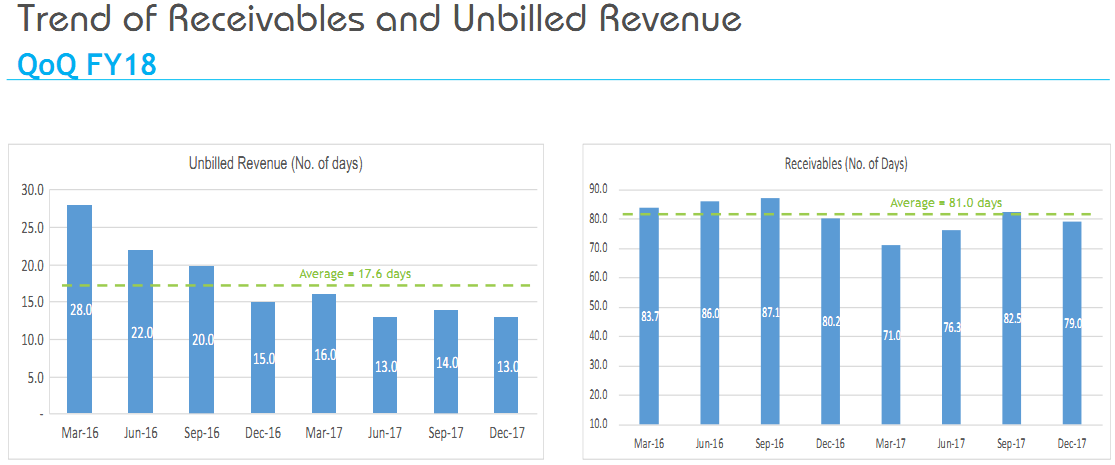

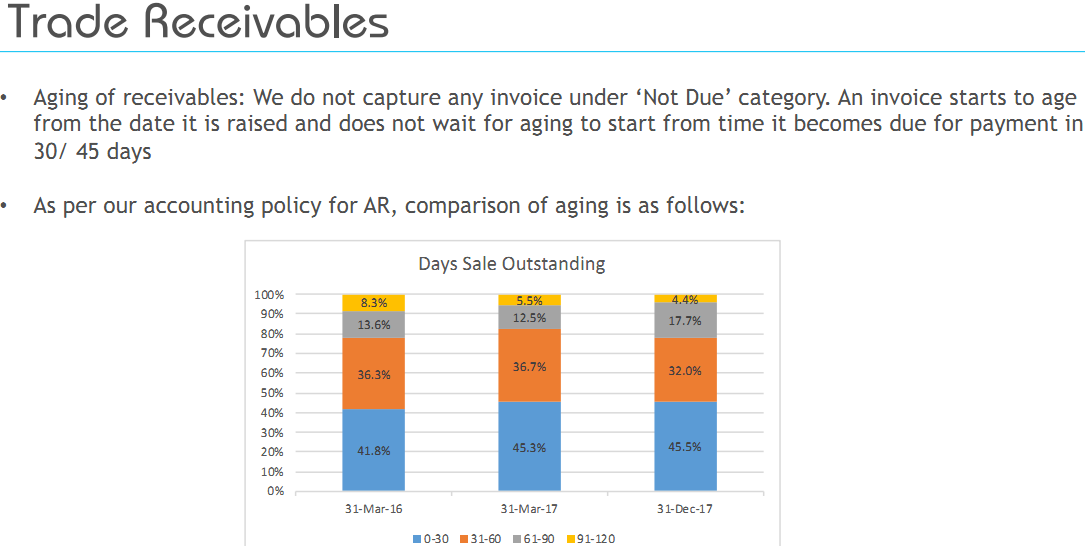

Looked at the PL and could not find any mention of “Receivables, Number of days” data? Is this disclosure mandated by Law? Why would the company cook up suspicious figures? To justify the high receivables in BS? Well, averages considered, there is justification in this high level as being due to the promptness of their billing! If “Unbilled revenue days” is now 10 days lower (lowest ever!) compared to Average, and “Receivables days” is correspondingly adjusted lower (for a fair comparison), then that gives an increase of only 13% over Averages.

So, either they are very creative crooks/cooks or are just plain with the truth.

OK, so the company financials are opaque to us. We do not trust Americano auditors but would like to deep dive ourselves into them. The superficial sign-off by Deloitte is insignificant.

Well, at least Deloitte has separated the Expenses clubbed together, so we could make educated guesses about the goings-on. “Depreciation&Amortization” and “Finance costs” are not changed but the other two items change!

Hi @vikas_sinha : great work at digging up the data !!

The whole problem with 8K Miles is that data points don’t talk to each other (or look practical). For example, NO permutation of Dec-17 aging profile provided by the company can produce an average Dec-17 receivable of 79 days !!! (similar is the case for other timestamps as well)

There are many such issues if you analyze further.

With all the keen scrutiny on the number being provided here, this stock does not deserve this kind of beating on the fundamentals. Every small observation is being used to paint a doomsday scenario. There is a perceived trust issue no doubt, but the numbers by themselves dont justify this kind of hammering. This price movement is clearly not linked to fundamentals.

If you stick to the argument that the results are all fake numbers then there is no point in further analyzing or discussing it at all…

Never mentioned that “results are all fake numbers”. I have provided my specific concern with rationale and if you want to address the same, you need to provide a relevant and data/logic backed answer which we can then analyze and discuss. These kind of blanket statements which try to brush aside any concerns or queries are not going to help anybody.

Financial diligence is a key part of any investment process and I don’t see a reason to abandon the same in this case, especially when there is very limited scope of on-ground research.

I have not seen any arithmetic that ties these various issues you speak of with the valuation. All these issues people are speaking of exist in reports of several companies and reflect genuine business challenges that all growing organizations face.

I can see only endless speculation on these perceived issues without anyone attempting to arrive at a logical conclusion. Can someone please link these issues arithmatically with relevant data/logic and explain what the right valuation should be. Or can someone arithmatically predict what impact these issues will have on future cashflow and show that the impact is outside the control range.

Whats happening here is not financial diligence but mere speculation and intelligent sounding gossip.

Let’s leave it here since you don’t seem to have specific answers to the concerns raised by others/me here. Let’s wait and see how the Q1 turns out - hopefully, cleaner and better.

Also, attaching an old piece of diligence by Ambit on 8K Miles - Ambit Diligence - 8k Miles. You might find it interesting to see how people invert, triangulate and identify issues.