They have not used any of the ‘phoney’ keywords listed by you AI/ML/IoT/Blockchain etc. Corporate (dis)honor is a very subjective topic. If management is aloof then that makes people jumpy, if management does con calls, interviews and provides updates to exchange, then that makes people nervous too.

These guys mention “cloud” since the years that Google jumped up on the AWS idea. I do not think anybody does any kind of mature MS tech .NET kind of solution without Azure incorporated into it. Cloud is nothing special much. These guys are trying to get a moat of sorts by a focus on healthcare business. I quote @tarunmahajan post just one above yours

balance sheet alone is not sufficient to judge a company otherwise all accountants would have been millionaires.

On a similar note,

AR alone is not sufficient to judge a company …

Discl: Invested since Oct 2017, average price of 340, 12% of PF. (60% done in past few weeks)

Fellow boarders, lets keep our discussions focused on inference derived out of data. There are several undisputed good things about the company.

Amazon, Microsoft has recognized the company under various categories of cloud recognition. They have put up the name of the company on their respective websites. Therefore we can infer without any doubt that company works on cloud platform.

All the subsidiaries are audited by auditors in USA. Those reports have been presented to Deloitte in India. Audits in USA are real. Therefore I trust the audited FY18 numbers.

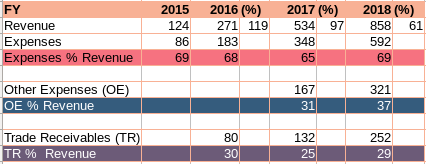

Based on FY18 numbers, the company is facing several challenges like quarter-on-quarter growth in q4fy18 has slowed. But year-on-year company has grown by 60% (fy18 vs fy17) It had, beyond a doubt. We need to look at q1 numbers which are on 8/Aug to see how does future look for the company.

Trade receivable have increased, yes they have. They are at 29% of revenue.

Company showed some contractual employee on it’s rolls. Looks like, it did.

Lets us try to judge the company objectively. Let’s no surrender all our faculties to fear because if that happens we will never be able to invest ever again. The company is growing at rapid pace and this kind of growth comes with several challenges, several hiccups. Investors have to take risk on management’s capability to overcome those challenges and move forwards. Some might fall in the process, of course some will.

Going by the PL statements of the past few years, this is probably one of the best performing IT companies in India. At a P/E of 7 (EPS 55) and Y0Y close to 50%, this scrip should be trading much higher.

But as evident from the discussions on this board, and the stock price, there are questions on the veracity of the balance sheet and the investor confidence is very low. Instead of speculating, we should ask and get written statements from the management on all potential issues. I wonder if AGM is a good venue for doing that but am not sure when it is conducted.

As some of the investors are planning to go to Chennai office, it would be good to have some concrete questions to help them. I’ll start with mine, others please add:

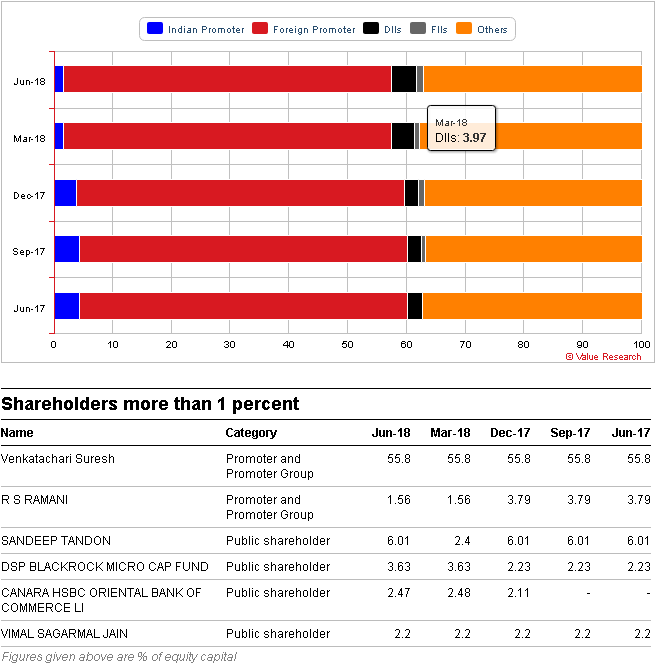

To increase investor confidence, will all the US subsidiaries be audited by Delloitte in the coming quarters.

To increase investor confidence, will the financials of each subsidiary be published separately.

Reason for the significant jump in trade receivables to 252 crores in March 18 quarter.

Reason for the significant jump in trade receivable days to 104 days in March 18 quarter.

More details on Other expenses (2.d of P/L statement). This is significantly high at 321 crores. It is much more than employee expenses of 235 crores which is typically the highest expense component for IT companies.

More details on Other Intangible assets (1.d of Balance sheet). There is a significant jump from 61 crores in 2017 to 225 crores in 2018.

Yes, “good value” I would say. The downside is limited I believe, hence the safety and growth factor in valuations.

An SME IT company, trading at PE of ~6, with consistently (very) high double digit growth in all aspects, most importantly in PAT, adequately experienced management, DSP Blackrock invested with 4% stake, early mover in sunrise industry and high potential of growth focus (health/pharma on cloud).

Discl: Invested since Oct 2017, average price of 340, 12% of PF. (60% done in past few weeks)

As I am quite new to Investing and accounting background and have not enquired any company before,I am requesting for any investors from Chennai to accompany me.

I am available in Chennai most of the weekends

The points you mentioned are the ideal recipe for disaster. The 8K miles of 2018 is way different from that upto March 2017.

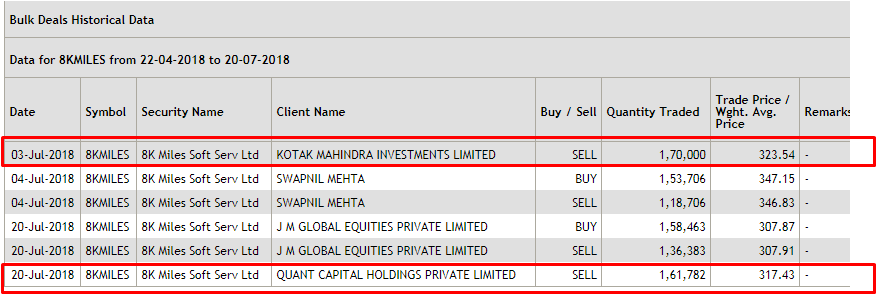

Some boarders are trying to breathe fresh air into the stock by belittling the balance sheet issues (debt, loans lent, receivables, disappearing cash, share pledge etc), assuming that price movement means nothing and instead focussing on the low PE, SMAC potential etc. PE is an incorrect way of valuing stocks and until this is understood, the stock will appear a value buy with minimum downside risk. Those stuck @ Kellton have the exact same arguments and they continue to load up.

If the management actually responds favorably to these requests that you list out, that’ll assuage the lost trust. Mind you, investors have lost “trust” and not merely the “confidence” based on stock price movement. The real investors know better how to value stocks and how to “behave” when prices decline.

I had mentioned my doubts about 8k Miles and provided rationale for my avoiding the stock in the past on June 1 when the stock price was near 600 levels, long before the current big fall. I had mentioned my doubts about the subsidiary accounting couple of times late last year as well when the stock price was around 900 levels. Even the latest post after results was before the stock moved up big on Monday and so had nothing to do with what the stock price is saying.

My first post on Fiberweb was in Sept last year when the stock was at its peak.

In Vakrangee it was when the stock was trading 6-7x higher than current price and in PC Jeweller, I had speculated money laundering due to demonetisation when the price was 5-6x current price. I am appalled by this sort of blanket statement brushing down apprehensions and doubts. I remember that you had the same problem on Vakrangee thread as well in the past back in early Feb. It helps to be open to views when holding a stock and to question one’s belief and not be blindsided by confirmation bias.

Appreciate your views on 8K miles on doubtful accounting. Here one things is that revenue of subsidiary of 8K miles is fake & bloated hence all profits shown may be fake as well & overstated balance sheet is presented & 275 cr receivable may also be fake. I can see two genuine issues, one is higher receivables of 275 cr & 375 cr other expenses. As Deloitte has not done full audit of subsidiary things are not fully clear. Let’s see if some pictures get clear during Q1 results. DSP blackrock is still invested might bank on their due diligence.

I can not argue with someone who reject the numbers outright and think that auditors in USA have signed-off cooked books but people who can trust number can see the below.

My inferences are as follows -

Revenue growth YoY is slowing down from 2016. At the same time revenues are growing. So revenue slowdown is not a new phenomenon, it is happening from few years. Inspite of slowdown, this growth is something.

Expenses as percentage of revenue are hovering in the range of 65-70% for last four years.

Other expenses as percentage of revenue have increased slightly. There is a case for some (not all) “body shopping” here. (Now do we distrust TCS, Infy - given what we know about “body shopping”) Can we live with it, given the growth of company?

Trade receivable as percentage of revenue have not increased suddenly. They are in 25-30% range for the entire life of company and given the competition in cloud space, I will say 25-30% trade receivable gives me confidence that numbers are real.

If we look at company’s numbers for year they clear lot of doubts. Market is not kind to small, mid-cap and that is causing havoc. Fear is setting-in and objectivity is loosing it’s place.

It’s far better to expect repayment in 2 years than it is to expect it in 10-15 years.

It’s still not bad to expect repayment in 10-15 years, but if you have to wait

70 years to break even, there could very well be something that could

go terribly wrong during that time. I’d invoke the inner Graham inside me

and just say no instead of hoping that the earnings catch up and nothing

goes wrong.

There’s enough historical evidence to suggest that paying a high price for

something good usually ends with paying an even higher price for

nothing good enough. I’d rather be safe than sorry.

@rvetri: while @phreakv6 has clarified his position, on my part - I had started raising concerns around Dec-2017 when 8k Miles was at ~900 - at all time high and NOT when it has fallen by more than 60% (you can check all my posts in this thread). I have been intrigued by its growth profile for long and started having concerns after the maiden quarterly result concall.

Now 8k Miles’ stock price may still go up, the fact remains that none of us have clarity and answers to a lot of business related questions which are required for making a sound investment decision. Answers to many critical questions have been defensive and on the lines of “balance sheet is not enough to judge a business”, “AR alone is not enough to judge a business” which gives little comfort to fellow valuepickres/investors.

I am just hoping that management got unfortunately caught in aggressive accounting practices for the last couple of years and is now in the process of cleaning up its books (for last couple of quarters).

Hi @Gaurav_Agarwal: for #1 to #4 of your post, if you look at quarterly numbers it actually gives a very different view. Question here: Any specific reason as to why you would not look at quarterly numbers which is a leading indicator for a business (Yearly numbers are generally better for seasonal businesses)?

@vikas_sinha

They have used all the above keywords (in press release & presentation both). And to give some background, 2-4 years back they were “cloud” only. After that “AI/ML” came in the presentations and press releases. And lately they have started including “blockchain”. Might be genuine as well but just thought of clarifying.

If you ignore the price movement for a bit and look at the business strategy 8K appears to have adopted, I believe their journey starts to make sense.

8K started in an environment and in a business segment that could have been breached by larger players with ease. Plain vanilla cloud adoption is no rocket science and all major players have been doing it since VMWare launched its products (much before AWS). I remember implementing VMWare based virtualization in early 2000.

so I ask myself, what strategy would a company adopt to survive the environment and competition.

Start by picking a niche which is a small-medium business unit in larger competitors; and go unnoticed by competition - 8K picked healthcare which is highly regulated and difficult to break into. Traditional services players focus less on highly regulated segments because there isn’t much bang for the buck if you are providing traditional IT services.

Build stickiness and dependency but focusing on products/IPs as opposed to services - 8k miles invested in assets that added value on top of what the base cloud products provided. This IP (intangible asset) driven value addition creates stickiness and dependency.

Grow rapidly and inorganically to a critical mass (in terms of assets, capabilities, and revenue) before the competition knows your there; if the competition notices you early you will stagnate - 8k chose to rapidly acquire skill and capability through acquisitions; that would have taken them decades to grow organically. The side-effect of these acquisitions was the crazy YoY and sequential growth seen so far.

Now that you have the moat of assets and capability, shift focus to organic growth - 8k now has the capability and assets to grow steadily but surely and are much better placed to face competition. Also, they are wise enough to realize when to stop the acquisitions and shift to organic growth. There are several startups that grew rapidly by growing debt and then realized they did not have the ability to manage the spread. case in points Educomp.

The problem is that 8k miles got discovered by the market too early and got caught up in crazy/frenzied price movement.

My take is that 8k is poised for steady and solid growth going forward, and the stock market has not yet caught onto that. Shareholders below 2L capital are dwindling rapidly while Institutions are cautiously increasing stake.

I have been adding 8K to my portfolio bit by bit at every price crash for the past 3 years and my bet is on their business strategy and less on their growth.