I am not advising you anything as there is no free lunch  .Its your money after all and if you feel 8k miles,Dilip buildcon and the likes worthy enough to invest then do so. You have every right to express your opinions the way I did. While you have written not to take personally, but would have been better if you had implemented the same while writing.Nonetheless, wish you good luck.

.Its your money after all and if you feel 8k miles,Dilip buildcon and the likes worthy enough to invest then do so. You have every right to express your opinions the way I did. While you have written not to take personally, but would have been better if you had implemented the same while writing.Nonetheless, wish you good luck.

2 Likes

if you see the charts, the stock moves extreme north and south in short times…not my kind of script

Yes , the amount mentioned in trade receivables is being recorded as PAT. When the cash is received, receivables are decreased and operating cash flows increases.

If that is the case,increasing receivables is not a RED flag to me , as long as net CFO is almost equal to net PAT

You are partly right; the CFO generated correlating with PAT should either go into building assets or find its place on the balance sheet. Since the overseas subsidiaries audit was done by other auditors and consolidated accounts only ‘consolidate’ those statements, it does not give confidence on the cash being generated. The true test is actually cash in the bank account!

Hopefully with IndAS consolidation, this may change.

completely operator driven stock it is … within 2 weeks it moved 100% sometime back.

BTW Are the promoters from Hyderabad ? I am just wondering why would list in India , when you can list in the U.S .

Its completely based out of u.s.They buy U.S companies as well.

Its is hard to con there vs here ? Might be one of the reason.

3 Likes

1 Like

Company is mulling about buy back @600. This will end the speculation about the existence of cash r not. Even in the IIFL interview Suresh talked about it in the fag end. If it crystallises it’s a big mover.

Here is the relevant part of the interview where buy back is discussed.

It says open market buy back up to Rs.600,

There are indications of promoters’ holding being hiked. How do you plan in this regard?

We plan to increase stake through creeping acquisition by purchasing from open market upto price of Rs600 per share

I would wait till buy back is done(if at all,it happens) and consolidated q4 numbers are out .

Post that I will accumulate more shares

1 Like

Be cautious…

There is a substantial differences between what they r saying and what they r doing!!

1 Like

Results awaited today

Things to be checked from the report

If the amount of receivables have reduced and whether the company has collected the actual cash

If the company announces buyback @ 600 as mentioned by CEO in a recent interview

The list of major Clients to the company and their contribution to the revenue

PM strips is no big secret, it is prominently quoted in Forbes report on this company.

"Suresh holds 55.8 percent stake in 8K Miles, which was first listed on the Bombay Stock Exchange in 2011 through a reverse merger with dormant Hyderabad-based company PM Strips Limited, and then got listed on the National Stock Exchange in 2014. (Dormant companies, also called shell companies, are often used as vehicles for various financial moves.)

“I don’t fundamentally like the venture capital model where they have a control over the business,” says Suresh, adding that a few investment bankers [who he doesn’t wish to name] advised him to go in for a reverse merger with a shell company.

Was it a right decision? “No. Absolutely not,” he says. “It took us about two to three years to clean up the image of that company. We should have waited for around two to three years and gone in for a new IPO or could have listed ourselves in the US markets where we would have got a much better valuation.”

A US listing for 8K Miles is something Suresh does not rule out. At an “appropriate time” he says either an American Depositary Receipt issue or a direct listing could be considered. “Currently we are growing significantly and gaining at least two large customers each quarter. Once our revenue excedes $100 million it would enhance our overall value.”

If 8K Miles gets listed in the US, it would be the second company that Suresh would take public on the American bourses, after SolutionNet International’s 1999 Nasdaq listing.

In the India-listed 8K Miles, there are no major institutional investors apart from DSP BlackRock Microcap Fund, which holds a 2.23 percent stake.

In fact, 8K Miles came into the limelight when DSP BlackRock bought over 3 lakh shares (approximately 3 percent stake) of the company in the open market at Rs 175 per share, in August 2014. Since then, the company’s shares have tripled to Rs 564.45 apiece as on April 24, 2017."

DSP BlackRock has increased stake in March '18 quarter (by more than 50%). As also, Canara Life, by absorbing the large majority of outflow from one promoter.

Discl: Invested since Oct 2017, average price of 340, 12% of PF. (60% done in past few weeks)

I ignored the P/L and went straight to the B/S and these are my observations.

-

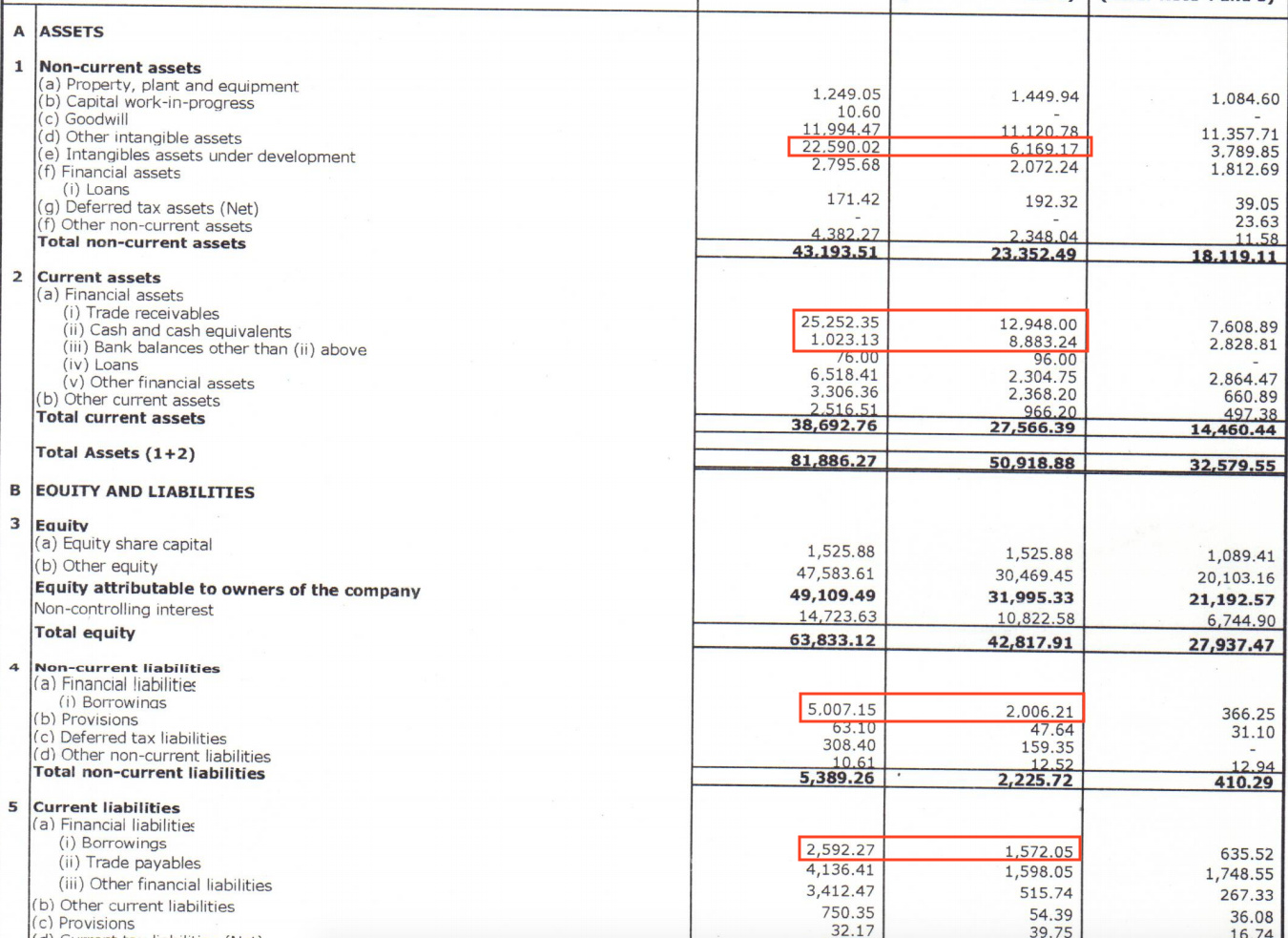

Receivables almost doubled YoY while sales only increased by around 60% in the same period. Current receivables stands at 252 Cr.

-

88 Cr cash has gone from the B/S and is now only about 10 Cr.

-

Borrowings up by about 40 Cr (Updated from 50 Cr I had incorrectly put earlier).

-

Intangible assets have increased almost 4x from 62 Cr to 226 Cr.

For a company thats not paying dividends and is converting whatever cash is in its B/S (and add to it the debt) to intangible assets via acquisitions, it is hard to believe that the sales are real considering the rise in receivables for a business of this nature. I continue to believe that this company is cooking its books.

11 Likes

Borrowing up by 40 Cr, right instead of 50 Cr

Non Current - 30 Cr

Current - 10 Cr

1 Like

Since these results are audited and all subsidiaries have been audited. Audited results have been presented to Deloitte, we should be ready to put in more work and show it to the satisfaction of others before issuing such broad statement. Not that we can do anything about what do you believe in.

Trade receivable are 29% of revenue which are high but not alarming by any measure. Companies do have trade receivable all companies have.

Cash is gone - Cash in companies is for spending only. What is the use of keeping cash in the books.

Borrowings is up. Yes, companies companies do take loan. All companies do take loans.

All the above three seems quite normal to me.

As far as intangible assets are concerned. You expand on your point and I will work with you to see, what does it mean?

5 Likes

Lot of negative aspects are up - Other Intangible Assets (61 to 225), Trade Receivable (129 to 252), Cash drying (88 to 10), Loans going up (23 to 65), borrowings up (current and non current), Trade Payable (15 to 41)more than doubled, Other financial liabilities (5.1 to 34) gone up by almost 7 times.

2 Likes

Debt/equity is only 12%, other fundamental quantities are within limit. No need to worry in terms of fundamental of the company though some of the parameters have increased significantly.