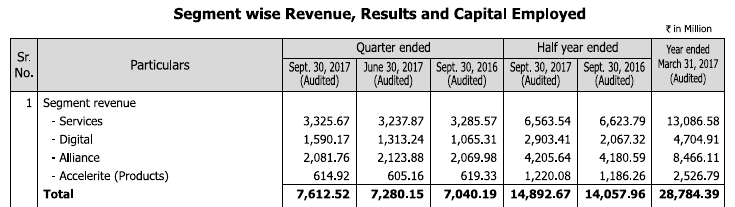

The growth in Digital and cloud is real. We have this confirmed from multiple sources (all source are public). Data from such varied source must be trusted. Today Persistent Systems released its data. According to revenue break-up only digital is growing and growth is close to 50% year-on-year.

You have raised a very valid point. Few years back there used to be a technology company which became education technology company . I can see lot of similarities but not claiming ,risk is always a possibility until it occurs and one has to draw his own line. The similarities are:

-

More than 80 percent revenues from foreign subsidiaries which were unaudited

-

Very high Revenue growth along with high receivables

-

Lot of acquisions and hence no free cash flows

1 Like

I second his thoughts i have been singing this all along when it used to trade at 80 PE and people bashed me on this view.

Same happened with me recently. Even after losing money if people don’t want to listen to you then its better to keep quiet.

1 Like

Keeping quite is a great strategy. People who believe in stock stories can

constructively debate the plus and minus, but with proof. People who don’t

believe in a stock story are welcome to criticise but should give proof.

Statements such as two or three of the employees of a big 4 co was

incompetent and Satyam happened, and so wherever the same big 4 firm is an

auditor, all those cos are in suspect etc…is not a good debate…It is

like saying a Boeing flight crashed, and so we should not travel in any

boeing made flight…And then an airbus crashes and people stop travelling

an Airbus…If we take such positions, the whole world can never travel…

4 Likes

Hi Dhruva,

Nobody here wants you to keep quiet. We actually like when somebody raises valid questions which helps us in validating/negating our thesis.

I guess many of us (including gaurav, myself, rvetri) expressed our thoughts on your concerns regarding growth, business model (pure salesman vs partner), revenue model (30%-40% already recurring instead of your original assumption of non-recurring revenue only), promoters profile (“they not being bunch of MBAs”), automation being already used (instead of your assumption of it being in the future), Big 4 auditors being appointed.

Of course, your concern on acquisition based growth (“using money to generate money”) is well placed. But that’s a level of risk which some people are willing to take looking at highly mis-priced valuations and growth ( and in the absence of any actual evidence of shenanigans) and some people are not. This, I believe, is the risk appetite which differs individually and is a part of small-cap/mid-cap investing.

Would love to hear more concerns/risk factors from you on this stock.

3 Likes

i have implemented cloud solutions for some time. i know the challenges, and can vouch that it is not easy for IT biggies to just come in and perform. Skills needed are deep and concentrated. So far, typical IT skills were available and wide-spread. So, edge was more in execution capabilities, and processes, to execute well. But in cloud projects, ‘proven’ skills (from projects execution) are more or less concentrated at onsite locations, not easily available at offshore. And also, smaller cloud-focused companies are ahead of the curve, compared to biggies. Hence, these smaller but experienced companies are able to make a headway whereas biggies can’t.

Trends - Experienced techies would understand that whatever opportunities that Suresh has talked on this BTVi interview (IoT, Helathcare Compliance Opportunity, Bots etc) makes sense, and that it most probably, will play out.

Financials - i have spent some time, and did not find most concerns valid.

CashFlows have not been good, but is understandable as they have made so many acquisitions, and also may not have been stringent or confident in asking for stricter payment terms. Even then, their receivables are in line with peers.

Price manipulation - was related to old pre-reverse merger promoters, that had moved out the year after reverse-merger.

Dividend fiasco - was unfortunate, but am not surprised if they did not have a strong non-tech team in place, and this happening.

But going by last investor presentation, they seem to have woken up, and tried to generate confidence. Also evident by appointment of Deloitte as statutory auditors.

All in all, I see this an opportunity that most of market participants won’t easily ‘get’, and due to often cited corp governance issues, ignore this stock… Until 1) some marquee investors buy into it, or 2) when it gets good valuation from US listing. or 3) when growth is visible in cash flows.

As to risks… of course, need to keep watching receivables, and cashflow improvements.

At this time, I remember what Samir Vartak explained in a recent interview on CNBC-TV18, that benefit of fast-growing companies, is that even if growth slows (say, from 35% 25%), and hence P/E comes down (from say 25 to 20), resultant price will still be higher than CMP. Try to do some calculations around that :)… And that creates partial margin of safety / downward protection if we are wrong in our assessment.

Discl: Invested 6% of PF value, two weeks back, a day before AGM.

4 Likes

I have been reading the thread and it is quite a good a discussion.

What I get from the discussion is, there are 3 aspects here.

Firstly, the business side, The overall verticals company operates like digital, cloud migration, healthcare, all hot areas and definitely, there is huge scope for growth exists for genuine players. As many others have said and what I know is the business prospects are good and company will continue to get projects and customers. There won’t be any issue on demand side for next 3-5 years.

Secondly, the company’s moat in this area. Agreed, the business potential exists, but what competency is company building to be the preferred vendor?

For this, not much data exists on the surface. For this, we will have dig deep to find the employee skills, per employee revenue, employee salary’s, margins per deals compare to best companies in the industry. As % of sales Employee cost is lower and SG&A is higher for 8K Miles, compared to many peer IT companies.

Seems, 8K miles is spending more money on sales, and generally, this implies they are in a competitive market and is facing pricing pressures. This may also that company brand is not known that well among customers and company is spending a lot of money in getting the deals. This needs more details and a bit of red flag for me now with my current understanding.

The third part is of financial part, there are many red flags here, as quite a few have pointed out.

The company seems to believe in inorganic growth, and hence continue to acquire companies and burn capital. In the process, it seems the company seems to more keen on showing vanilla numbers like 100% revenue growth, account profit to keep the market happy and show their deals are good. Receivables are high and no sign of cashflow.

If we really want to bypass these financial red flags, then we will need a genuine answer on the business prospects and company’s competency of high skilled employees and ability to deliver complex projects and be the preferred vendor in the areas they operate. Until we know this, it is really tough to forgo the financial aspects of the company.

Disc: Not invested.

1 Like

@Prash Very well articulated. You are absolutely correct in saying that areas like digital, cloud etc are seeing huge demand and likely to continue for next few years. You are also right in saying there is a lot of competitive pressure.

I have spent over 20 years working in many large, mid-sized and small IT companies and one thing I can say for sure, all of them realize they need to be in this space and everyone is working on war footing to grab a large piece of the action. I don’t see technology or even execution itself being a moat . What is going to matter is the deep relationship you have with your customers as you need to understand the domain and business very well.

For a new comer, only way is to acquire companies with existing client. However, M&A strategy is always very hard to execute and mostly helps only in linear revenue increment.

Disc. Not invested in 8K Miles.

1 Like

@dheegarg you are right that building a deep relationship with customers is key. But how do we know that 8K miles is building that kind of relation?

As I see ticket sizes are mostly less than 3 million dollars and the company has to keep adding new clients regularly like any other IT company.

If there isn’t much moat in technology or execution, what stops clients from switching to different providers after taking initial service from 8K miles? Are there any metrics on how much business they are getting from existing customers vs new customers.

But I see that company has 600+ employees and in Q1 they had almost 195Cr revenue. So, revenue/employee is quite high compared to other IT companies.

Do we know how much of the revenue is coming from onsite vs offshore. For larger IT companies this is about 50/50. If onsite revenue is higher, this could explain higher revenue/employee.

Which peer companies have to take for comparison?

Trade receivable as percentage of revenue for financial year 2017 is 25%.

Consolidated Cash from operation from 2011 to 2017 is 150 crores whereas net profit for same period is 178 crores.

While you are saying Receivables are high. Most humble, high compared to what??

A leader in the field is Microsoft partner 8K Miles.

1 Like

@Gaurav, thanks for pointing out.

For comparison, I would like to take IT company’s who are into consulting as well as services. Be it biggies like TCS/Infosys or mid-segment like persistent, zensar.

May be 8K miles is not a pure service company and are more in to consulting level. Hence they have more cost for sales and per employee, revenue is higher.

No doubt, they are showing profits and there is operating cashflow exists. But, to do this, they also had to issue additional shares. Share capital has increased 3 times. Again the numbers right now seem, their investment is paying off. It is a bit risky bet.

Receivables, you are right. It is not at an alarming situation.

About the preferred vendor, right they have all the right partnerships with Amazon, Oracles, Microsofts of the world. But on the customer side, how do we know they are most preferred. I am not sure if being preferred vendor’s for cloud companies by itself is a moat. Though it is a significant achievement.

Technologies like Cloud, Devops, Continuous Integration and Deployment have reduced the need for manpower therefore comparison with TCS/Infosys is not like-to-like. Size or segment does not matter here, we need to look at IT companies with different perspective.

I do not find comparable company in India in listed space, therefore I have looked beyond and the following companies looks comparable to me

- Twilio

- ServiceNow

- Workday

- BulletProof

Financials of these companies are freely available on Google Finance. Just to remind you 8K gets 80% or its revenue from US operation.

I think you are talking about two bonus given by the company on 15/May/12 & 24/Aug/16 in the ratio of 2:3 & 1:3 respectively and a split done on 24/Aug/16 from face value of Rs. 10 to Rs. 5.

We should actually call-up some vendors talk to them.

I use two of the products you listed here and with 100% confidence say they are far superior product companies unlike a service provider 8Kmiles is.

Both of them are SaaS offerings helping their customers lower/eliminate cost of ownership of IT infrastructure and are examples of using cloud to disrupt traditional product vendors in the same space. These are companies leveraged cloud from product inception and wouldn’t never need an 8k to help them.

ServiceNow - Comprehensive suite of IT infrastructure management software that is hosted on cloud

Workday - Human resource management software hosted on cloud

their business is similar to a gmail or salesforce

Who needs services of 8k

- Any IT product startup wouldn’t required help of a company like 8k,

- large conglomerates with products would have inhouse teams helping with migration to cloud because if you need to rewrite the codebase, 8k can’t help

- The services they offer might help companies having physical IT infrastructure running software to run operations and can be categorized to three;

a) but they are better of migrating to products that run natively in cloud (eg workday, service now, salesforce, outlook etc)

b) cloud infra can be costlier if you lift/shift existing stuff

c) those who realize and fall for the hype of moving to cloud can either charter 8k or any of the IT consulting companies (I see no moat)

disclosure : I don’t own 8k, I do have good experience with datacenters/cloud

1 Like

Right, this would be best. If we can find companies who are using or evaluating 8K miles product/service and what other companies they are comparing with 8K miles.

I

I never said these companies are 8K customers. By “Comparable” I meant companies with which you can do balance sheet, profit and loss and cashflow statement comparison/analysis to reach a certain or close to certain conclusion of some aspects of business.

You will agree that comparing Infosys/TCS/Wipro will not be useful. If you can suggest better comparable companies, you are most welcome to do so.

You above analysis inevitable leads to conclusion that services of 8K are not needed in market. But contrary to you conclusion company is clocking unparalleled revenue growth which implies somebody needs their product/services and is paying for them.

Below find short list of customers of 8K, then we can together thing why these companies would have hired 8K

sutter health

hawai pacific health

blue cross blue shield

shire pharma

big pharma company

listed in lse

nawaz shah wrote testimony on website

alchera

stanford health

deaconess

the queens medical center

kaiser permanente

lancaster general health

city of hope

the chopra center

rady children

jeppesen

As far as these names are concerned… I personally know that four in this list are world class hospitals, based out of SF Bay Area/ Silicon Valley. Of which, one is my primary healthcare provider.

Sutter Health, Kaiser Permanente, Stanford Medical, Blue Cross Blue Shield

The selling of 1.5L shares is not by promoters. The selling was done by MV Bhaskar, former director of 8K Miles, who ceased to be a director since 2013.

Please see the attached disclosure.

1 Like

I presume former director should have a better understanding of business & company than anyone of us here …