As per the latest annual report the only two promoters are Mr. Suresh and Ramani. I am not sure who is Mr. Surna, report doesn’t speak about him as a promoter

Article is about erstwhile promoter (Dipin Surana) and not about current promoters. Current promoters ( Mr. Suresh Venkatachari & R.S. Ramani) had acquired “8k miles” somewhere in 2011-12 for getting their company listed on exchange. So wouldn’t see this as irregularities with the existing set of promoters.

Disc: Invested.

On the face of it, it appears like a great value. But I have had seen similar numbers with another Chennai based company before - Helios Matheson. When it appears too good to be true, invest a 5th of what you want to invest is what I do and if it works out well, you know when to increase the stake and if doesn’t work out, you don’t lose your shirt!

Past delinquency (as noted before by others) is the cause of concern and moat identification is not easy for a small time investor - I am not sure why it should be difficult for an established player to get into this field of work and the only moat I see is the momentum of focus (healthcare and manufacturing) that could provide natural business opportunities. But large IT companies have healthcare practice as well as cloud practice and I can’t figure out why they can’t smother 8K…

Disc: Tiny investments right now. It looks promising, but not yet convinced.

1 Like

Even though IT services companies are facing a challenging environment (more on this in a minute), they do have significant moat which can be proven by their excellent margins and repeat business which could be 80-90% of annual revenues.

The reason for moat is that once they build applications/systems for any business, they not only have proprietary knowledge of the business, they are the only ones which know the inside-out of these applications. Hence it gets very expensive to change vendors quickly.

However, in my view, cloud transformation by itself does not provide the above benefit. And most IT companies are anyway providing these services to their customers.

With regards to my earlier point that IT services companies are in a challenging environment, it seems primarily due to following two reasons (there could be more):

-

Availability of cheaper/on-demand Saas based software has significantly impacted application development and maintenance work, which so far used to be the biggest revenue generator. Further, infrastructure management work stream is also impacted due to migration to cloud.

-

Most businesses today are facing challenges due to technology disruptions and new business models. Amazon, Uber, Facebook, Google’s of the world have been making in-roads into even traditional industry. This has somewhat impacted the IT spends by traditional industry.

Disc: Not invested in 8K miles nor intend to do in near future

Do you think any Indian IT company is leading in these new gen areas? I am looking to diversify by buying a very good IT stock not bothered by these legacy issues. What do you think about LandT infotech.

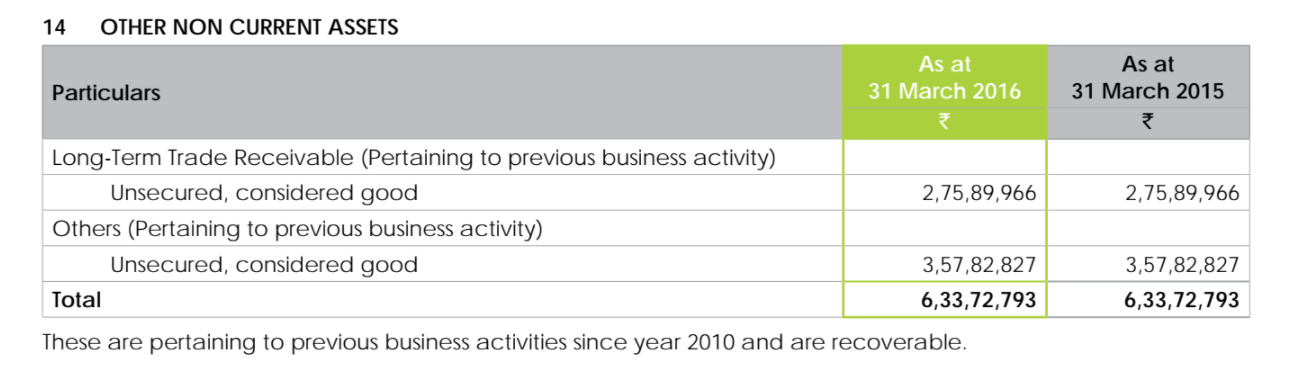

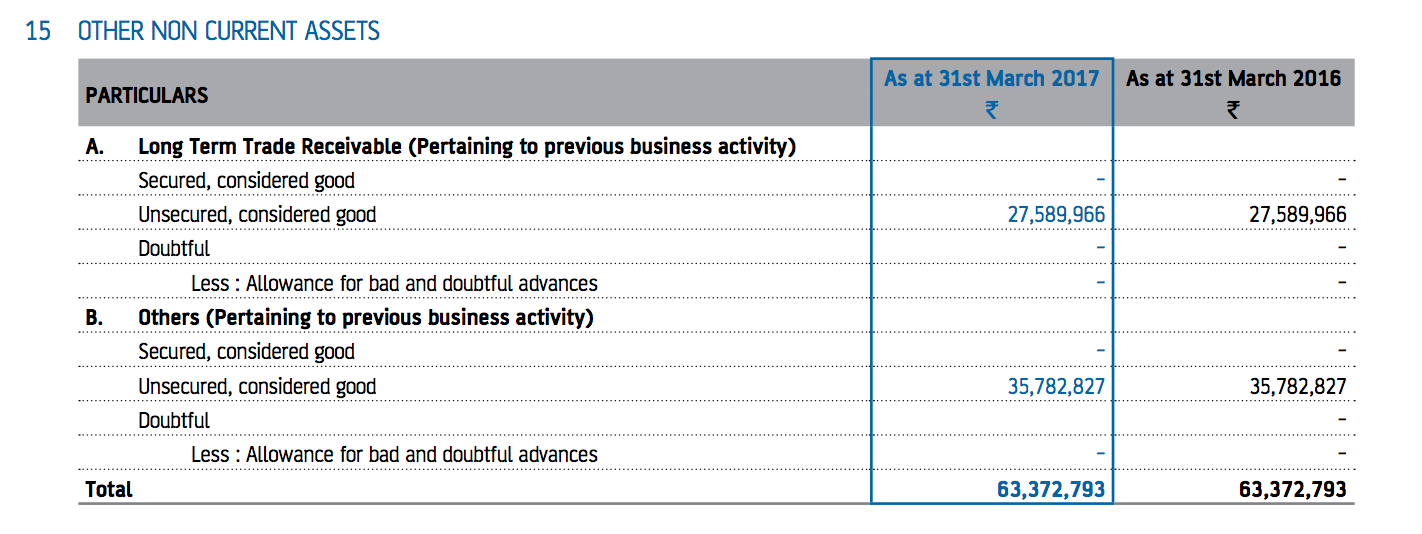

Sill carrying recievables considered good from 2010; but this AR seems to have dropped the fact that these are old receivables.

2016 AR:

2017 AR:

Companies like HCL, Wipro, Infosys, TM, TCS will have this practice. 8K miles appears to be one of the companies whose sole focus is doing the cloud migration.

While going through the Annual Report-2017 came across this (page 16, Case Study):

As per annual report, client is using 8k Miles’ SaaS MISPTM (Identity Service Platform).

On further digging, it turns out that the client is Oracle corporation (several sources below confirming the same description).

source:

“Oracle”

"Oracle Corporation - Wikipedia "

“Corporate Facts | Oracle”

2 Likes

It is surprising that the Co. is classifying 7 year old receivables as good and not providing for it. If it turns out, that the receivable has to be written off, then it will not be a tax deductible loss, as the business to which it pertained, has been discontinued. Hence, the entire 6.3 cr will hit the bottomline.

1 Like

Forget accounting and taxation,use accounting to look at character of company.

BTVI Beyond The Bottomline Mr Suresh Venkatachari Chmn & CEO, 8K Miles 12 oct 2017 28min 14sec

Passionate talk by the Suresh of how he started, what cloud computing and 8K Miles is all about, its future etc.

1 Like

Bloomberg anchor was speaking about brokerage notes/reports which stated $ 200 mn as the near term revenue goals (24-30 months mentioned by Mr. Suresh Venkatachari later). Does anyone happen to know which brokerages have covered 8k Miles and issued reports ??

Naz… USD 200 M was a guidance by the MD Suresh… I do not think it was

from a brokerage report

@rvetri

Agreed, it is eventually a guidance given by MD Suresh.

But if you listen to the Bloomberg Anchor (at 0:13 ) in the video shared by Gaurav above, the anchor specifically says - " i think if i look at all brokerage notes, they say that from the current revenue size that you have, you aim to reach $ 200 mn in the near term and eventually $ 500 mn as well"

So I guess, after the recent analyst/investor/brokerage firms meetings, some brokerage firms have issued reports/notes which the bloomberg anchor was referring to.

Isn’t Amazon , Microsoft, Google , Oracle etc working on seamless migration to cloud services ? What is the moat 8K has ?

I believe they are more like a salesmen for Amazon , Microsoft, Google , Oracle etc to companies which know nothing about cloud. You can call it consulting but for me it is salesmen thing.

Its like a broker who shows you houses available for rent in new city (as you have no idea about city ) and makes the cut from you or owner.

They don’t have any recurring revenue model. I was wonder all along why it was trading at 80 PE back then .

The future cash flow cannot be predicted because they are brokers , its purely supply demand thing i don’t think what they are doing is so unique that other IT companies can’t do …

If you have still not come out of the 2014 growth hangover i would recommend please do so…

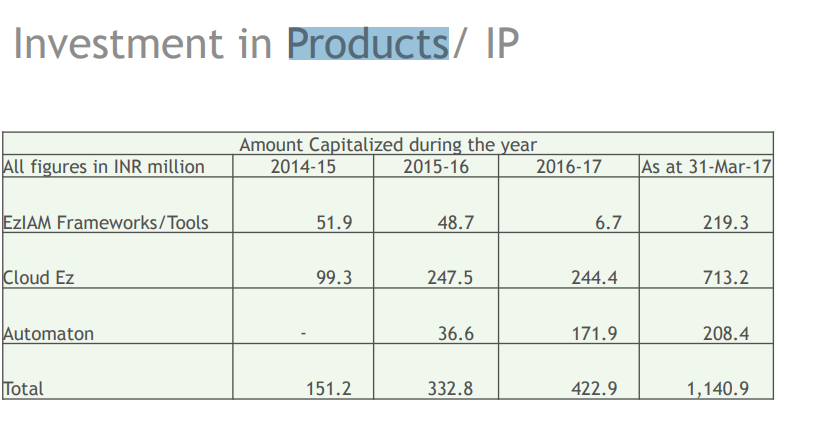

Now 8k has started talking about building products some bot AI and some analytics tool , which could be a painful journey .

Thanks,

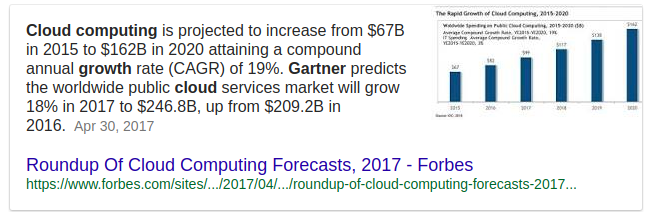

Why do you think the growth in Cloud Migration is over? The revenue of company grew by 88% to 196 crores in first quarter of financial year 2018 compared to last year first quarter.

I will most delighted if you could mention one industry (not company) projected to growth at such rate!

They already have products. Bots are part product called Automaton (the product is ready and operational, management demoed during analyst conference in Mumbai)

1 Like

Very apt comparison of the broker (8k Miles) and owner (Amazon) of the new house (Cloud Infrastructure). Here, broker is actually doing following tasks:

-

Consulting Revenue Stream: advising which house is suitable for their needs depending on size, amenities, cost etc.

Duration & Revenue type: Duration is about 2-12 months and revenue model is one time/order-book type consulting revenue. -

Cloud Migration Revenue Stream: new house set-up and helping Clients in shifting

Duration and Revenue type: few months to 4-5 years for enterprises and revenue model is one time/order-book type long term project revenue -

SaaS offering & Security Solutions Revenue Stream: Providing new furniture, household items (white goods), security systems on a pay-per-use basis

Duration and Revenue type: This is the recurring revenue model -

Managed Services Revenue Stream: Maintenance of the house for any eventual electricity outage, water shortage, domestic items break-down, emergency etc

Duration and Revenue type: This is also recurring revenue model

So, they do have recurring revenue model as mentioned above.

Although, they start as pure brokers/salesman providing consulting/shifting services for a one time fee, they eventually continue as managed service provider and SaaS/Security solutions providers with recurring revenue model (more like facility management companies in non-technical world with bots/automation doing the management/maintenance work providing non-linearity in the business model).

Disc: Invested.

5 Likes

Hi dhruv,

I think you are right they are brokers and salesman mostly and may provide some solutions also for their customers. But that doesn’t mean they can’t have recurring revenues, the customers pay recurring fees and so they could get a recurring revenue/commission from them.